United States

United StatesThe bifurcation between public and private credit markets has widened more starkly than anticipated.

The two private credit failures that prompted our October note now look less idiosyncratic and more diagnostic. The collapse of US auto-parts supplier First Brands and sub-prime US auto-finance and used-car business Tricolor – with combined liabilities exceeding US$11bn – has been followed by indictments against executives in both businesses for defrauding lenders.

Longstanding concerns that limited disclosure within private credit can obscure true leverage and conceal deteriorating credit quality until it is too late, appear to have been validated by these high-profile – and high-value – cases. Recent redemption requests have forced some private credit managers to restrict withdrawals.

Against this backdrop, the possibility of contagion into public high yield markets cannot be ruled out.

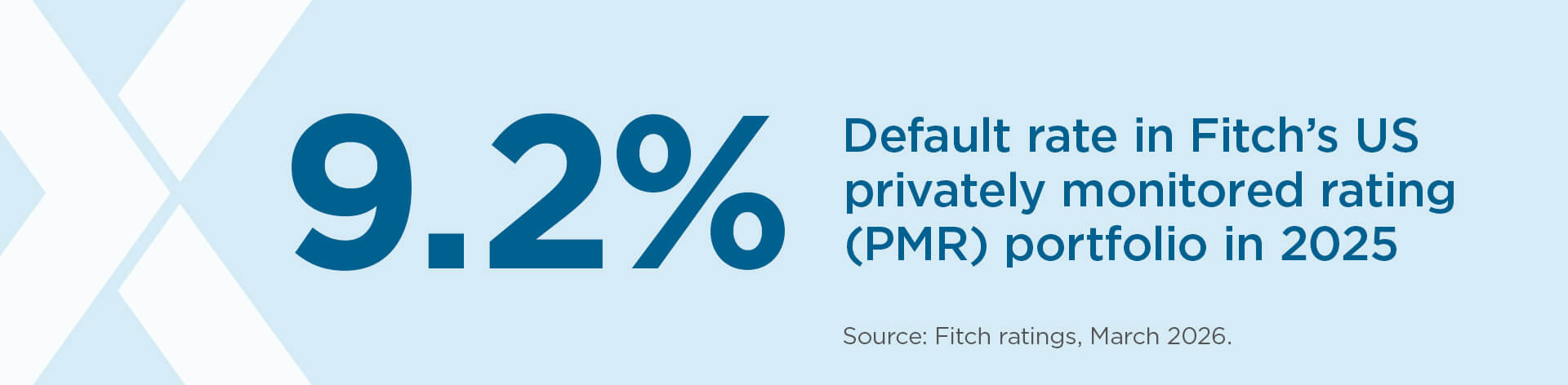

Defaults are rising – in private credit

Within private credit, Fitch estimates default rates at 9.2% in 2025 – up from 8.1% in 2024.1 Credit rating agency KBRA has meanwhile observed that documentation in upper-middle market direct lending has continued to weaken.2 Morgan Stanley has forecast that the prospective shakeout within private credit could be on a scale comparable to the pandemic.3

Within public credit, the trajectory has been very different. US high yield bond default rates remain near historic lows, at around 3%, with most credit losses concentrated in individual situations rather than sector-wide stress.4

Spreads to government bonds have moved within a narrow range and remain close to all-time tights: the US high yield option-adjusted spread sat at around 272 basis points (bps) on 29 May 2026.5 We believe it is telling that high yield spreads have widened only modestly since conflict erupted in the Middle East, disrupting global energy markets and pushing up inflation, while spreads on new private credit issuances have widened from the mid-400bps to around 500bps.6

The migration of the lowest-quality borrowers into direct lending and broadly syndicated loans, which we flagged in October, has if anything accelerated. The global high yield index is now tilted towards ‘BB’-rated bonds (the highest non-investment grade rating), duration sits near historic lows (at around three years) and the debt maturity wall has been pushed out to 2028 and beyond.7

Crucially, the high yield market is also supported by corporate fundamentals that have held up despite the rate environment.

Redemption queues and gates

The first significant test of the non-traded business development company (BDC) structure came in the first quarter of 2026. Quarterly redemption requests across several of the largest perpetually non-traded vehicles ran at roughly twice the standard 5% quarterly cap. Several large private credit managers, including BlackRock, Cliffwater, Morgan Stanley and Stone Ridge, enforced their gates against requests.8

In February, Blue Owl Capital took the most consequential step in permanently restricting redemptions from one of its main private credit funds and announcing a shift to a drawdown model, with capital to be returned over time. This is the first major non-traded BDC to be effectively gated outright since the structure became a mainstream retail product.

In one sense, the structural guardrails are functioning as designed: redemption caps, bank credit facilities, liquid asset buffers and maturing loan principal have all helped contain the pressure on private credit.

Recent events have, however, made visible something that was previously implicit: quarterly liquidity in non-traded BDCs is a promise that holds in benign conditions and is suspended when stressed. ‘Mark to myth’ valuation concerns appear to have been validated.

Investors who priced these structures as substitutes for liquid credit are revising that assumption. The result has not been the systemic event some feared, but it has driven a meaningful re-rating of the wrapper.

A time for caution, not complacency

The case that we made back in October – that public high yield offers more disciplined disclosure, more reliable valuations and a higher quality borrower mix than the rapidly-expanded private credit market – has, in our view, been reinforced by recent events.

This is not a moment for complacency, though. Public high yield credit valuations are tight, spreads do not offer a generous margin of safety, and dispersion is rising.

We remain cautious on more highly leveraged parts of the market, particularly issuers exposed to consumer cyclicals and payment-in-kind (PIK) ‘toggle’ structures, which grant borrowers flexibility to alternate between repaying in cash or adding interest to their debts. We are also closely watching for any pick-up in dividend recapitalisations as private equity sponsors seek liquidity routes.

The risk of contagion from private markets into public has not closed, and the past six months have widened the cracks in private credit that would carry that risk if it were to develop.

1 Fitch Ratings, March 2026. Based on Fitch’s US privately monitored rating (PMR) portfolio

2 Kroll Bond Rating Agency, April 2026: Q1 2026 Middle Market Borrower Surveillance Compendium

3 Fox, M., 17 March 2026: A ‘significant’ private credit shakeout on par with Covid losses is coming, predicts Morgan Stanley. CNBC

4 Fitch Ratings, March 2026

5 Bloomberg data, as at 29 May 2026

6 Hamilton Lane, April 2026

7 Bloomberg data, as at 22 May 2026

8 Association of International Certified Professional Accountants, April 2026

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.