United States

United StatesFears about the health of private credit have erupted following two high-profile corporate collapses in the US this September. Consensus is that other failures will follow: to quote JP Morgan chief executive Jamie Dimon, “when you see one cockroach, there are probably more”.

While each failure may appear idiosyncratic, together they hint at structural fragilities in the private credit market, which has never been tested at its current scale through a full credit cycle.

For public market investors, contagion is the risk. If collective wisdom determines that private credit dynamics pose a systemic threat, a self-fulfilling downturn in credit – and especially within high yield – could ensue. By no means is this inevitable, though.

Fundamentals within high yield credit are robust, with historically low default rates supporting tight spreads over benchmark yields. Generally strong corporate credit fundamentals provide comfort on public credit valuations, overall, as the warning signs on private credit ring loud and clear.

Two failures, one pattern

Global assets in direct-lending and private-debt funds have surged since the global financial crisis to around US$3tn.1 The sector flourished in the low-rate world as banks pulled back from corporate lending and investors chased yield, encouraged by claims of double-digit internal rates of return.

But rapid expansion appears to have come with familiar late-cycle traits: covenant-lite structures, aggressive profit adjustments and rising borrower concentration. What once looked like flexibility – limited disclosure and bespoke terms – now looks more like complacency following two high-profile failures.

On 10 September, sub-prime US auto-finance and used-car business Tricolor Holdings collapsed into liquidation with more than US$1bn of liabilities amid allegations of double-pledged collateral, falsified reporting and worsening loan quality.2

Shortly afterwards, on 29 September, First Brands filed for Chapter 11 bankruptcy protection with more than US$10bn in liabilities after years of debt-fuelled acquisitions and opaque financing.3 The US auto-parts supplier had borrowed through a fairly complex set of mechanisms including trade finance, asset-based lending, broadly syndicated loans and off-balance sheet financing.

Both indicate that a lack of transparency within private markets can obscure true leverage and conceal deteriorating credit quality until it’s too late. They may be the first visible cracks in an edifice built on optimistic assumptions about recovery rates and default correlation.

The fact is that unless the underlying loans are publicly traded, private credit valuations are a matter of opinion, not fact, and volatility will be underestimated. Talk of 100% positive returns needs to come with a health warning that private asset valuations may be more ‘mark to myth’ than reality.

Market ripples

Collateralised loan obligations (CLOs) are one mechanism through which the impacts of private market collapses may be felt.

Neither First Brands or Tricolor is large enough to pose systemic risk. As public market credit investors, our main concern is therefore the possibility of contagion.

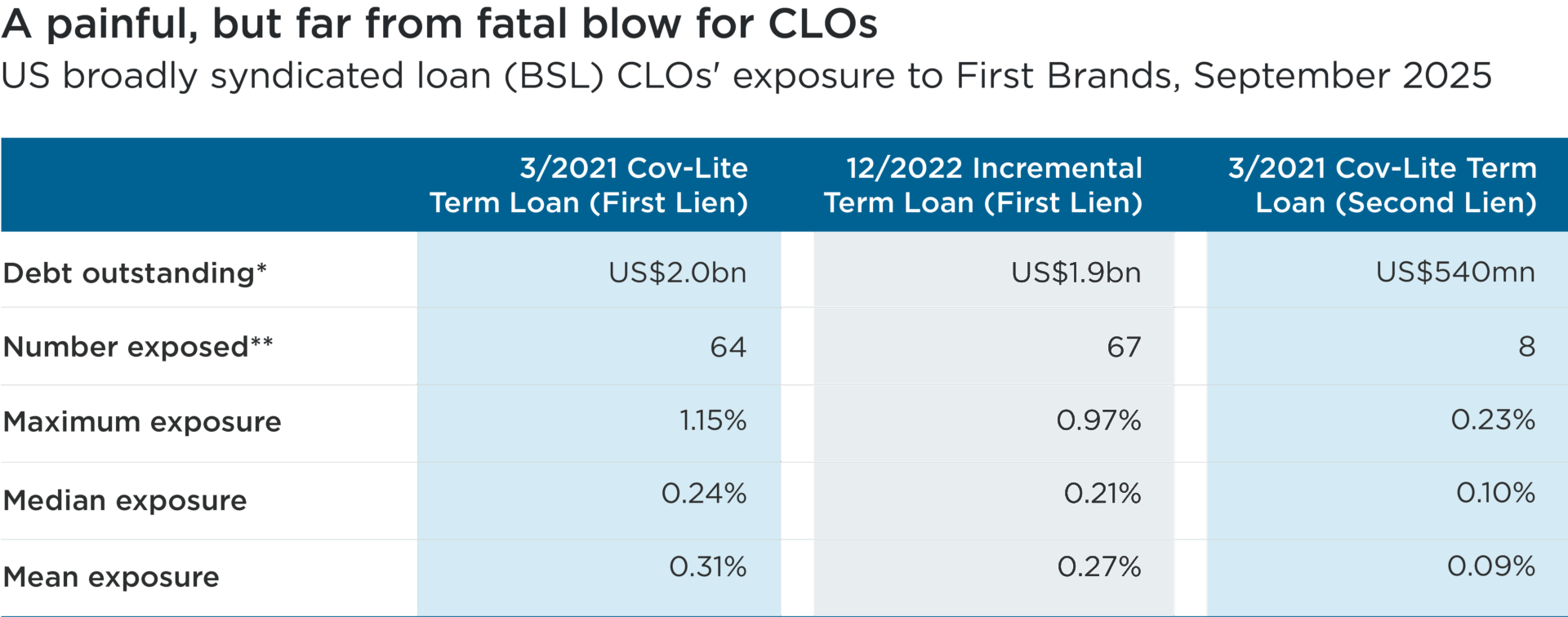

First Brands was a large issuer of broadly syndicated loans (BSL) bought by CLOs, whose portfolios are managed on a highly diversified but largely model/rules driven basis. While First Brands credit exposure was sufficiently modest not to trouble senior investors (see the table below), the losses will undoubtedly hit the returns of CLO equity holders including managers and sponsors of the vehicles themselves.4 In turn, this reduces the first-loss cushion enjoyed by the senior parts of the capital structure. The US$2tn leveraged loan market is highly dependent on, and inter-related with, the CLO investor base which now owns over 60% of the loan market.5

Source: Bank of America / Bloomberg / Intex / Markit, October 2025

* As at 30 June 2025

** Out of a total of 148 US broadly syndicated loan (BSL) CLO managers

The First Brands default not only reverberated through CLOs but also private credit closed-end business development companies (BDCs), regional banks, trade finance specialists, insurance companies and credit funds, triggering a hunt for where the credit exposure resided. Even managers with no direct exposure have reported a shift in tone among allocators – a new risk aversion after years of complacency and weak underwriting standards.

Most analysts insist the damage is contained: exposures are generally manageable and credit events to date have been largely idiosyncratic. But the reassurance has a familiar ring – ‘isolated defaults’ in the early stages of past credit downturns were later recognised as early warnings.

When lenders scramble to verify assets or enforce claims, contagion becomes as much psychological as financial. Private credit funds depend on confidence in valuations and underwriting standards. If investors begin to doubt portfolio marks – especially in funds promising quarterly liquidity – redemptions and markdowns could feed a self-reinforcing cycle of tightening credit.

Some institutional investors are already re-examining their allocations to direct lending, and banks are reassessing warehouse lines and counterparty exposures. The result could be a mini-credit crunch within private markets, potentially spilling into public debt through reduced bond issuance and higher risk premiums.

Robust fundamentals in high yield

More highly leveraged capital structures and weaker business models will be tested as the credit cycle eventually turns. High yield credit therefore intuitively looks most vulnerable to the fallout from private markets.

However, credit quality has improved markedly in recent years: more than 60% of the global high yield market is rated ‘BB’, compared with around 40% two decades ago.6 This shift within high yield towards larger, higher quality issuers has coincided with the growth of private credit and broadly syndicated loans, suggesting that the highest-risk borrowers have migrated to those sources of lending. High yield bond markets therefore arguably represent the highest quality place to invest across sub-investment grade credit markets.

Moreover, the proceeds of high yield issuance are primarily being used for refinancing, rather than corporate activity. Against this backdrop, we remain vigilant for signs of increased use of high yield bonds in dividend recapitalisations as private equity sponsors face increasing pressure to look for ways to return capital to investors. Given the maturity of the credit cycle, we are also cautious on more highly leveraged parts of the market exposed to the consumer and the use of payment-in-kind (PIK) toggle notes. Generally though, balance sheets remain fairly strong, in a historical context, and US high yield bond default rates are near historic lows – accounting for only 0.49% of the index over the past 12 months.7

In the context of elevated all-in yields, these factors all help support global high yield spreads to government bonds which are close to all-time lows.8

The end of easy credit

Notwithstanding the strength of the high yield market, the risk of contagion cannot be entirely dismissed.

The failures of First Brands and Tricolor reflect strain in the plumbing of private credit: in monitoring, collateral validation and accountability. The extent of their fallout depends on what follows: rising defaults, tighter liquidity and shaken investor confidence will, given the scale of private credit and its de facto role as the marginal source of corporate finance, likely leach into public markets.

For now, they do mark a turning point. The era of easy money, hubris and opaque lending is giving way to one of scrutiny, discipline and recalibration. Credit investors – public and private alike – would do well to listen carefully to the warning and focus on the fundamentals.

1 Morgan Stanley, October 2025: Understanding Private Credit’s Rapid Growth

2 Sen, A., Azhar, S., & Tracy, M., 14 October 2025: Auto sector bankruptcies spark fresh scrutiny of Wall Street credit risks. Reuters

3 Saini, M., 16 October 2025: Mapping the scale of beleaguered First Brands’ debts and its creditors. Reuters

4 Fitch Ratings, 6 October 2025: U.S. Leveraged Finance and CLO Weekly

5 LCD, as at 31 December 2024

6 Impax analysis of Bloomberg data, 22 October 2025

7 JPMorgan Default Monitor, as at 1 October 2025

8 Impax analysis of Bloomberg data, 22 October 2025

Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point, and Impax Asset Management shall not be obligated to provide any notice. Forward-looking statements or forecasts herein are subject to known and unknown risks and uncertainties including inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. . While Impax Asset Management has made reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.