United States

United StatesThe fixed income landscape has fundamentally changed. For much of the post-2008 era, credit strategy was largely a function of loose monetary policy, tight credit spreads and duration management within a broadly disinflationary environment. Many institutional investors turned to private credit, trading illiquidity and transparency for additional perceived yield.

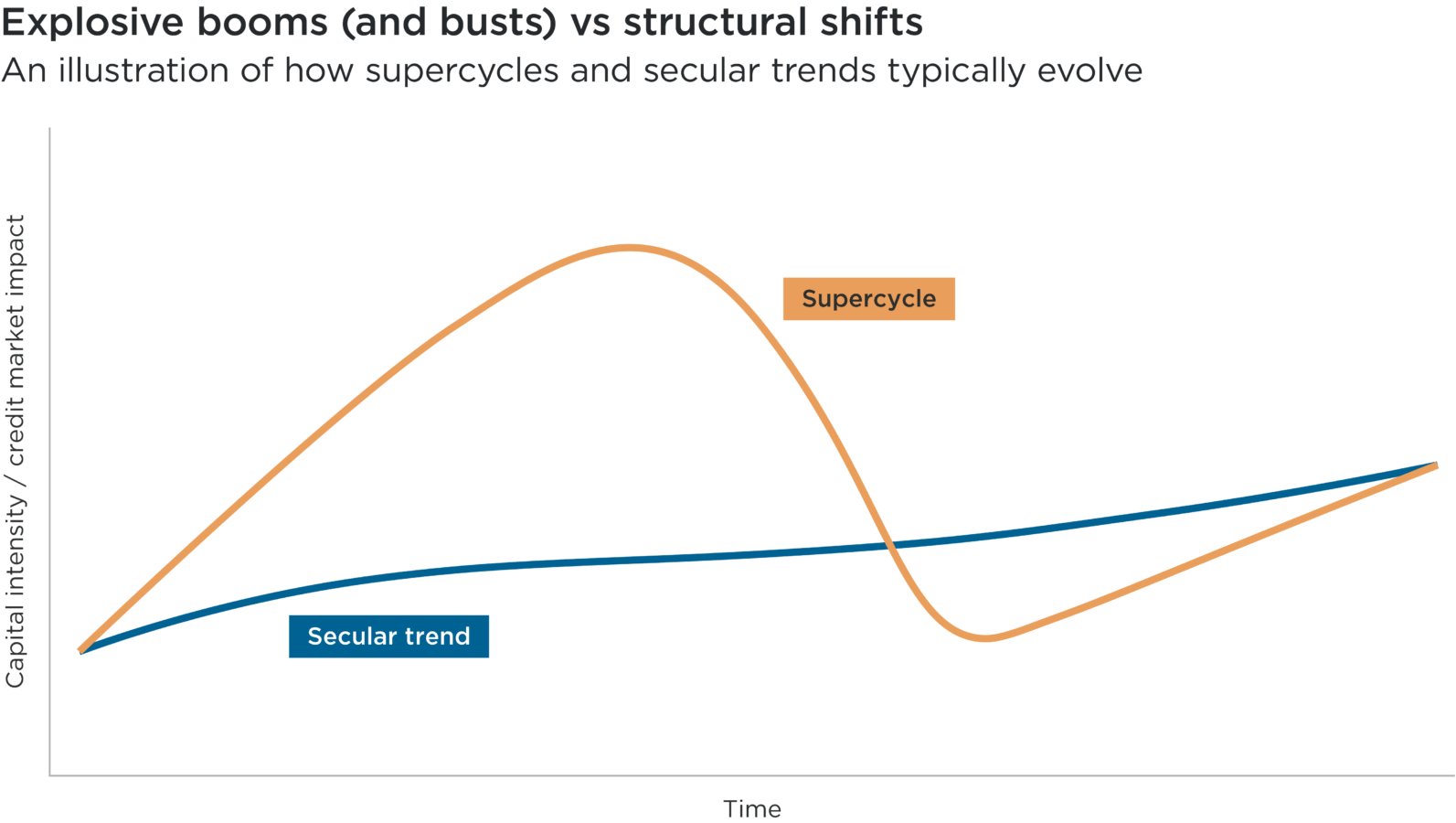

That era is over. In its place, a new architecture of structural forces — comprised of ‘supercycles’ and ‘secular trends’ — is reshaping the risk and opportunity set across global credit markets.

We identify four supercycles and four secular trends that can be practically embedded into credit strategies, from sector allocation to issuer selection, covenant analysis and portfolio construction. Understanding and incorporating these forces is no longer optional: we see it as the foundation of a durable, forward-looking investment process.

The framework: supercycles versus secular trends

The distinction between a supercycle and a secular trend matters enormously for credit investors, particularly around the timing and magnitude of capital deployment.

A supercycle is characterised by capital expenditure (capex) requirements that span decades and run into trillions of dollars. For credit markets, supercycles generate sustained primary market issuance, create new issuer categories – for example in securitised credit and impact bonds – and produce differentiated credit profiles between incumbents and new entrants.

However, supercycles rise and fall over time, and sometimes crash. As credit investors, we need to ask, “who captures cashflows and who gets over-leveraged chasing the theme?”.

A secular trend, by contrast, is a slower-burning, behavioural and structural shift in how economies and societies function. These are not necessarily characterised by the same explosive capital formation as supercycles. For credit investors, secular trends tend to influence the credit quality trajectory of existing issuers, the defensibility of revenues and the long-term resilience of business models.

Source: Impax, March 2026. For illustrative purposes only.

Supercycles: where capital flows and credit opportunity concentrates

We believe that credit investors should treat supercycles as generators of ideas: to identify emerging and cyclical investment opportunities or threats. Four stand out to us, above all.

1. AI and automation: the infrastructure imperative

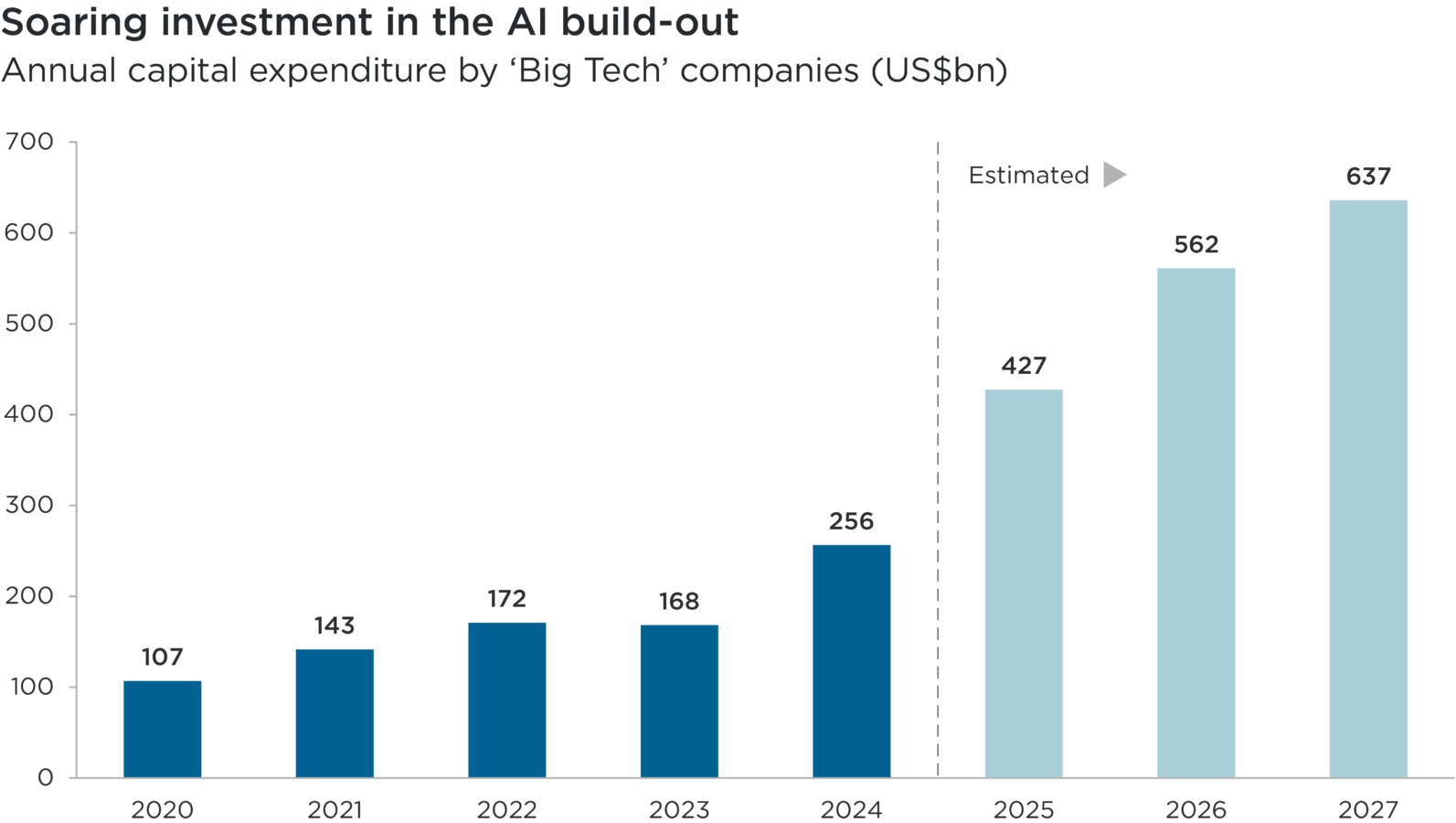

The AI supercycle is perhaps the most acute near-term opportunity in investment grade and high yield credit. The primary driver — ’intelligence’ as a new factor of production — demands a physical infrastructure build-out of extraordinary scale: data centres, GPU (graphics processing unit) clusters, power substations, cooling systems and fibre networks. It is creating a deep and expanding universe of investable credits.

It is key to distinguish between direct or derivative beneficiaries of the supercycle and outdated, ossified business models. Direct beneficiaries include the ‘hyperscalers’ and co-location data centre operators, both of whom are actively issuing investment grade paper to fund expansion.1 Derivative beneficiaries include utilities supplying power and water to data centres, construction materials suppliers, semiconductor and memory producers, and specialist equipment manufacturers.

Within this infrastructure stack, credit investors should be stress-testing issuer balance sheets against the capital intensity of the build cycle and monitoring whether free cash flow conversion can support the debt service implied by ongoing capex programmes.

Critically, this supercycle also creates risk for issuers who fail to adapt. Software, legal services, financial services, manufacturing and logistics may face increased uncertainty and meaningful margin pressure from AI advances over the medium term — a secular headwind that should inform credit quality assessments in those sectors.

Source: Bloomberg data, January 2026. Figures for 2025 onward are estimates.

Subhead: Annual capital expenditure by ‘Big Tech’ companies (US$bn)

Overview: This bar chart shows the combined annual capital expenditure (capex) of the largest technology (‘Big Tech’) companies, namely Alphabet, Amazon, Apple, Broadcom, Meta, Microsoft, Nvidia and Oracle since 2020. Figures from 2025 onward are estimates.

Overall, this chart illustrates how ‘Big Tech’ companies’ capex more than doubled between 2020 and 2024, and is forecast to have more than doubled again by the end of 2026. This reflects a surge in investment relating to the AI build-out.

2. Energy security: the dual mandate

The energy security supercycle is being driven by two mutually reinforcing imperatives: decarbonisation and energy independence. Geopolitical shockwaves from conflicts in Ukraine and the Middle East have accelerated both, and the capital requirements — estimated in the tens of trillions globally — dwarf almost any prior infrastructure investment cycle.2

Credit opportunities exist across the energy transition capital stack including green bonds from utility issuers, project finance structures for renewable generation and storage, infrastructure debt for grid modernisation, and hybrid capital from legacy energy companies.

The intersection of AI and energy is also worth highlighting. Data centre power demand is now a material driver of new electricity generation investment, creating a mutually reinforcing dynamic between the two supercycles.

3 & 4. Water and food security: underappreciated capex cycles

Water and food security are arguably the least discussed, but most structurally compelling supercycles for credit investors with long time horizons. Both are driven by scarcity dynamics that are worsening as global populations rise, and as a changing climate disrupts historic weather patterns.3 Meeting growing demand for both water and food requires vast, sustained capital investment.

Industrial and agricultural water demand, and the cooling requirements of AI data centres, are driving significant capex – and debt issuance – from operators of desalination and water treatment plants and of smart grids.4 Investments in vertical farming, precision agriculture, irrigation infrastructure and food logistics are meanwhile also feeding new issuances.

Issuers in these related supercycles are often infrastructure-like credits with long-duration revenue streams, strong asset backing and inflation-linked cash flows — characteristics highly attractive to fixed income investors seeking real yield and diversification away from corporate credit cycles.

Secular trends: credit quality through a structural lens

Meanwhile, we identify four secular trends that should be leveraged as credit quality filters: to assess which specific issuers will be winners or casualties within those broader shifts.

1. Cybersecurity and defence: non-discretionary spending

Cybersecurity has crossed the threshold from discretionary IT expenditure to an existential business cost. For credit analysts, this reclassification implies that cybersecurity revenues are increasingly recurring, contracted and resistant to economic downturn. Issuers in this space — from software vendors to managed security service providers — therefore deserve consideration as defensive, cash-generative businesses. However, careful credit selection is paramount given potential AI-related disruption.

Meanwhile, rising geopolitical tensions have led to growing demand for defence-related products, including countermeasures against hybrid warfare and drone attacks. Military spending in Europe has risen as a consequence of regional conflict and pressure within the NATO alliance, and sees no sign of abating in the medium term.5

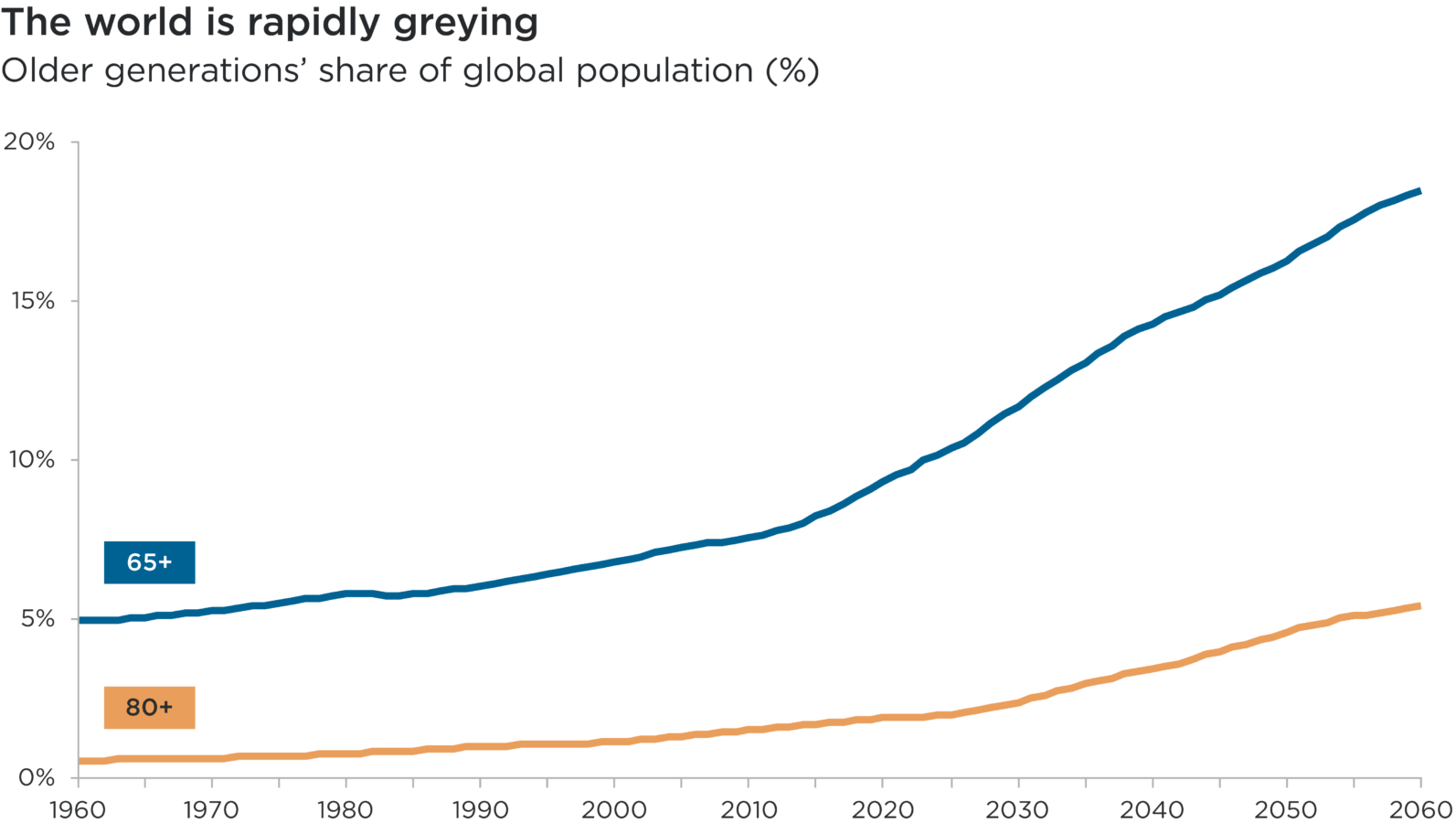

2. Demographics and healthcare: the silver tsunami

Ageing populations across the developed world are creating predictable, long-duration demand for healthcare services, automation and pharmaceutical products. Demographic trends support the credit quality of well-run healthcare operators and innovative pharmaceutical and medical technology issuers.

Conversely, it puts pressure on government credit profiles as social spending obligations grow and tax bases shrink.

Source: United Nations, 2024: World Population Prospects 2024. Figures for 2024 onward are estimates.

Subhead: Older generations’ share of global population (%)

Overview: This line chart shows the percentage of the global population that is aged 65 and over (blue line) and 80 and over (orange line), respectively, since 1960. Figures from 2024 onward are estimates.

Overall, this chart illustrates how these cohorts’ shares of the global population are now rapidly rising, having increased gradually since 1960. Based on demographic trends, older generations are forecast to form a significantly larger percentage of the global population by mid-century.

3. De-globalisation and regionalism: reconfiguring supply chain risk

The transition from just-in-time to just-in-case supply chains is one of the most far-reaching secular trends for credit investors.6 It implies significant capital reallocation: away from global logistics and towards more regional manufacturing, nearshoring infrastructure and domestic production capacity. Issuers deeply embedded in global supply chains — whether as operators or financiers — face margin and revenue risk as the model shifts.

Conversely, issuers building the infrastructure for regional supply chain resilience represent a structural growth opportunity that credit teams should be actively mapping.

4. Crypto and blockchain: institutionalisation and credit implications

The steady institutionalisation of digital assets is beginning to have tangible implications for credit markets — from the creditworthiness of crypto-native issuers to the disruption risk facing traditional financial intermediaries.

Credit teams should be monitoring this space, not as a speculative sideshow, but as a source of disintermediation risk for legacy banks and payment processors, and as a growing source of primary market issuance as blockchain infrastructure scales.

Integration into the investment process

These supercycles and secular trends are not a backdrop to the credit investment process; they should be core foundations of it.

At the portfolio construction level, we believe teams should establish explicit sector weights and thematic tilts that reflect the relative opportunity set across supercycles. At the issuer level, analysts should incorporate underlying exposures to secular trends into their credit framework — both as opportunity identifiers and risk amplifiers.

Covenant analysis should also evolve as capex cycles accelerate, credit agreements that lack appropriate covenants or capex limitation provisions become materially riskier. Duration positioning should account for the long-tailed nature of supercycle investments versus the reality of government fiscal deficits. For example, infrastructure and energy transition credits often have duration profiles that benefit from a steeper yield curve but carry refinancing risk in tighter liquidity environments.

Finally, integration of sustainability-related factors and thematic investing are increasingly convergent. Many of the trends outlined above are simultaneously credit risk factors and impact investment opportunities. Fixed income teams that build unified analytical frameworks to gain a more complete picture of credit risk will, in our view, have a structural edge over those treating sustainability as a separate overlay.

Ultimately, it is our conviction that fixed income teams who orient their credit strategy around these structural forces — and build the analytical infrastructure to exploit them — will be best positioned to generate durable, differentiated returns across the credit cycle.

1 Murugaboopathy, P., 22 December 2025: AI spending spree drives global tech debt issuance to record high. Reuters

2 International Energy Agency, 2025: World Energy Investment 2025

3 Intergovernmental Panel on Climate Change, 2021: Sixth Assessment Report

4 Global Water Intelligence, 2025: Rethinking Resilience

5 Stockholm International Peace Research Institute, 2025: SIPRI Military Expenditure Database

6 Bain & Company, 2024: Not-So-Distant Shores

Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point, and Impax Asset Management shall not be obligated to provide any notice. Forward-looking statements or forecasts herein are subject to known and unknown risks and uncertainties including inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. . While Impax Asset Management has made reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.