United States

United StatesIndustrial stocks are not thought of as defensive. Businesses in the sector are typically asset heavy, often relying on cycles of capital expenditure and positive economic sentiment for growth. However, suppliers of mission-critical and highly specialised components fly in the face of this stereotype.

Where such companies are embedded within the supply chains of high-growth industries, they can also present compelling long-term opportunities. Secular trends like electrification and artificial intelligence (AI) have helped drive indicators of economic confidence steadily upwards, despite new tariff regimes.

Against a backdrop of macroeconomic uncertainty, technological disruption and divergent valuations within global equities, we believe the sector contains some hidden and resilient gems.

Economic moats in mission-critical niches

There is no ‘one size fits all’ approach to investing in industrials. The sector accounts for almost 30% of our Environmental Markets universe.1 Companies within the sector range from suppliers of building products to operators of transportation networks.

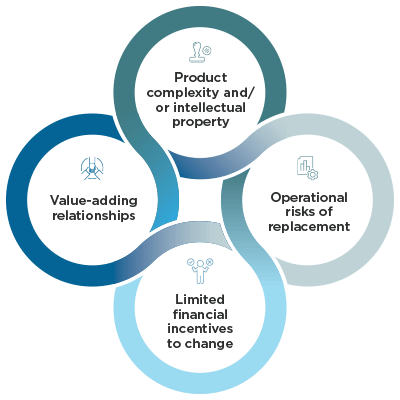

However, when looking for more defensive growth, one approach is to identify specialist companies that manufacture high value-add products and dominate their respective niche within an industrial supply chain. These can benefit from durable economic moats in four interrelated ways.

First, advanced components whose manufacturing involves significant complexity are often difficult to replicate or substitute. This may be because the technology is highly sophisticated or because equipment costs are prohibitive below a certain scale. Their design may also be protected by patented intellectual property.

Second, substituting existing suppliers represents an operational risk. By their nature, businesses cannot function without mission-critical components. The process of switching suppliers can entail pausing production and carries with it the potential for failure, both of which come at a cost.

Third, the financial benefits of switching may be modest at best. Within the context of complex industrial processes, the cost of any one component – however critical – can be very small as a percentage of the total. This can limit incentives for change.

Fourth, relationships often offer additional value. Many suppliers will partner with their customers throughout the product lifecycle, embedding themselves deeply in operations and aftermarket servicing. Such interdependence raises barriers to entry for competitors.

Source: Impax, 2026

Defensive exposure to high-growth end-markets

We believe companies that occupy this space within the value chain are well-positioned across economic cycles. In the boom years, they participate in the upside as vital components are designed into customer products and solutions. When times are more challenging, they are less vulnerable to price renegotiation and may even be able to offset weaker shipment volumes with after-market servicing.

We believe one such company is UK-listed Spirax Group, a specialist in industrial heat management which forms lasting partnerships with its clients. Its steam and electrical divisions provide energy-efficient solutions to a range of defensive end-markets including power generation, healthcare and consumer goods. By embedding its engineers within customer operations, Spirax generates around 85% of revenues from operational expenditure budgets, which tend to fluctuate less than capital expenditure (capex).2 Moreover, by optimising customer operations, the company improves both their financial and sustainability profile, effectively doubling the value-add. This has enabled Spirax Group to outgrow global industrial production in 13 of the last 15 years.3

Geopolitical ructions, including tensions over Greenland, have emphasised the resilient role that companies specialising in high value-add products can play in portfolio construction. While the US Supreme Court has now ruled that Donald Trump cannot impose wide-ranging tariffs under the International Emergency Economic Powers Act, he may yet pursue other avenues which prompt trading uncertainty and more stockmarket volatility.4

Xylem is a supplier of water treatment and related infrastructure. Its long-term growth is underpinned by rising demand for clean, safe water as well as increasing environmental pressure on existing systems. In recent results, the US-listed company’s management highlighted that the essential nature of its products gives it the pricing power needed to offset the impact of tariffs and inflation.5 As a result, management has been able to protect profit margins and improve earnings visibility. These qualities are highly prized by investors during times of elevated market volatility.

Within portfolios, makers of specialised industrial components can also provide an element of diversification. While their products fulfil a very specific function within a process, that process may have applications within various sectors of the global economy. For example, suppliers of critical grid components like Hubbell are participating in AI-related growth opportunities without being overly exposed to the trend.

The US-listed company generates the bulk of its sales from steadily-growing, regulated utilities and grid operators whose revenue base is expanding with the electrification of the global economy: the world’s grids are expected to double in length by 2050.6 Yet AI’s need for uninterrupted power at precise voltages has fuelled demand for Hubbell’s high-capacity connectors and modular power systems, with data centre-related sales in its Electrical Solutions division up 60% year-on-year.7 With capex by global technology companies expected to reach at least US$660bn in 2026, the opportunity set for Hubbell and other suppliers of critical electrical hardware is expanding.8

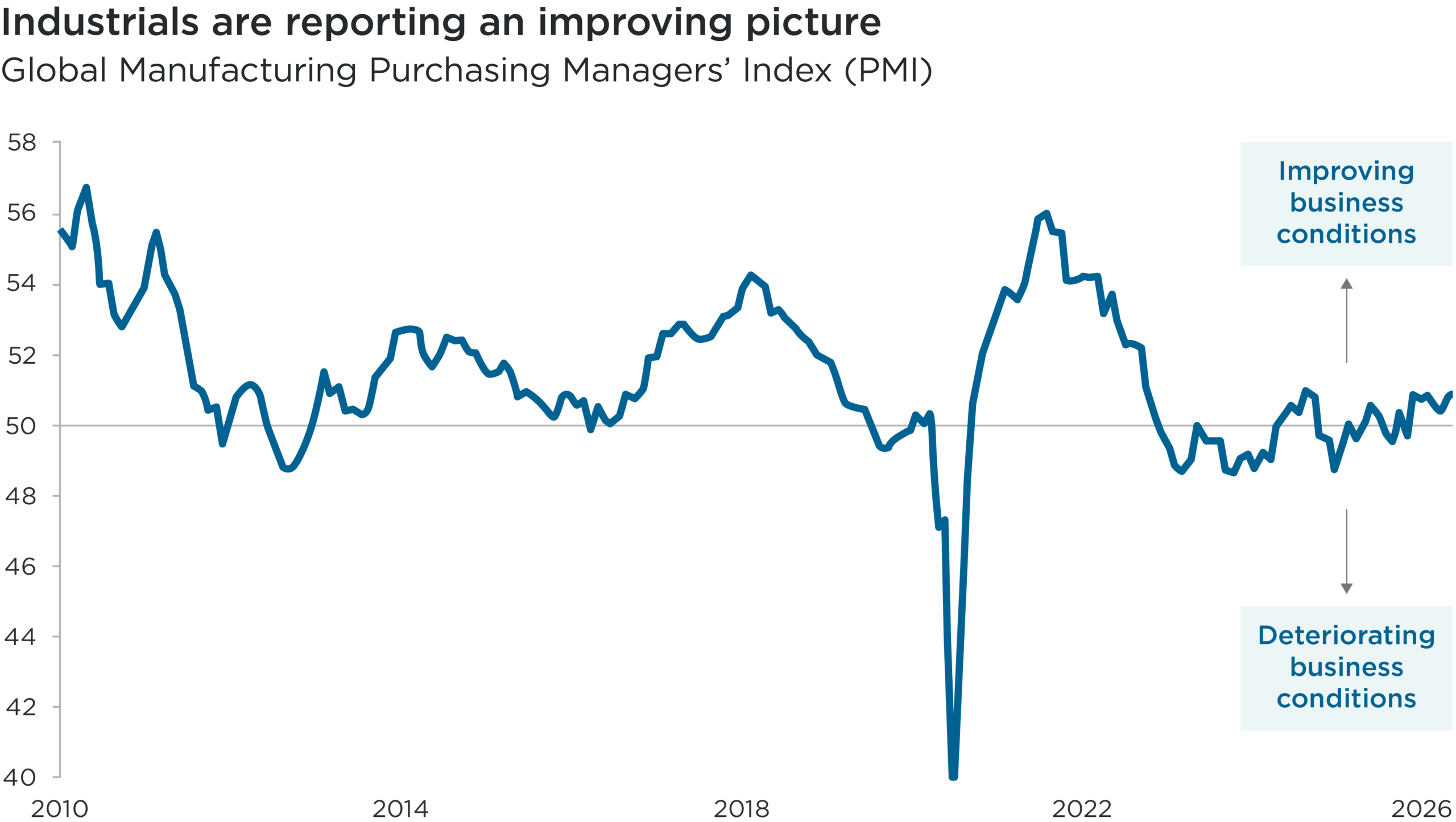

Source: S&P Global PMI with JP Morgan, February 2026. Data from January 2010 to January 2026.

50 = no change on previous month.

Subhead: Global Manufacturing Purchasing Managers’ Index (PMI)

Overview: This line chart shows the evolution of the Global Manufacturing Purchasing Managers’ Index (PMI) between January 2010 and January 2026. The Global Manufacturing PMI is based on a monthly survey of purchasing managers across the manufacturing sector to assess changes in business conditions. A number above 50 indicates improving business conditions, while a number below 50 indicates a deterioration.

Overall, this chart illustrates how business conditions, as measured by the Global Manufacturing PMI, have been on an upward trajectory in 2025 and into early 2026, reflecting a gradual recovery from their post-2022 slump.

An improving backdrop

We believe companies specialising in high value-add products, with strong competitive positions and exposure to structurally expanding end-markets, can play a key role in equities portfolios in the current climate.

Tariffs aside, the macroeconomic backdrop is improving for industrial companies. Following a prolonged cycle of inventory de-stocking following the pandemic, as well as higher inflation and interest rates, global manufacturing PMIs (Purchasing Managers’ Indices) have recently managed to sustain an upward trend (see chart above).

After years of exceptional stock market concentration, we believe conditions are ripe for a new dynamic based on corporate fundamentals and valuations. Industrial companies that are embedded within the supply chains of high-growth industries look well positioned to thrive, in our view.

1 Impax Asset Management as at 31 January 2026. The Environmental Markets investable universe is defined as companies deriving at least 20% of revenues from activities aligned with Impax’s Environmental Markets taxonomy.

2 Spirax Group, March 2025

3 Spirax Group, March 2025

4 Sherman, N., 20 February 2026: Trump brings in new 10% tariff as Supreme Court rejects his global import taxes. BBC

5 Xylem, February 2026

6 BloombergNEF, 8 March 2023: A Power Grid Long Enough to Reach the Sun Is Key to the Climate Fight

7 Hubbell, February 2026: Fourth Quarter 2025 Earnings Call

8 Morris, S., Acton, M. & Rosner-Uddin, R., 6 February 2026: Big Tech’s ‘breathtaking’ $660bn spending spree reignites AI bubble fears. Financial Times

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.