United States

United StatesGeopolitical risk has returned to global energy markets. Conflict in Iran and the resulting blockage of the Strait of Hormuz has pushed global oil, gas and electricity prices higher, underscoring how exposed modern economies continue to be to energy shocks. Even as an uneasy ceasefire holds, energy prices are likely to remain elevated and potentially more volatile.

Against this backdrop, the economics of energy management and efficiency solutions look more compelling. While higher energy prices can sap economic growth, they have historically catalysed investments in efficiency upgrades. We do not believe all companies stand to benefit equally from this opportunity, however, and investors need to be selective.

Energy prices look likely to be higher for longer

Conflict in Iran has sent energy prices surging. At its peak, Brent crude was up over 90% year-to-date, while European natural gas futures had risen over 130%.1

In electricity markets where gas is often the marginal source of generation, as in many parts of Europe and Asia, this has translated into higher wholesale power prices. German baseload futures, for example, surged 25% in early March.2

While oil prices have fallen since peace talks began, Bloomberg analysis estimates that they could remain as high as US$170 a barrel.3 Even in the event of rapid and total de‑escalation of the conflict, damage to energy infrastructure, combined with higher insurance costs and increased security risks for shipping, means oil futures are not pricing an imminent return to levels seen at the start of 2026.

Energy shocks encourage solutions

If Russia’s full-scale invasion of Ukraine in 2022 overturned post-Cold War complacency around energy security, this conflict has driven that message home. Fear of energy price volatility is once again a reality for businesses, consumers and investors.

Energy price shocks often prompt governments in importing countries to adopt measures that enhance energy security. This is only likely to increase as global electricity demand growth is turbocharged by the rapid expansion of data centres.4

As a relatively low-cost and scalable way to add domestic generation capacity, renewables are again enjoying policy tailwinds as they did after restrictions were placed on Russian gas exports: in 2023, the EU boosted clean-energy investment by roughly one-third, to around €360bn.5 This is not to say that governments are only looking to renewables to enhance energy security, however. Italy’s decision to slow its coal power phase‑out is illustrative of how system stability considerations can temporarily redirect policy signals.

Solutions that improve energy management and efficiency are less visible than renewables, but are also poised to benefit. This is because when energy prices surge, payback periods shorten, and economic participants are highly incentivised to adopt technologies that disrupt the normal relationship between GDP growth and energy consumption. For example, when oil prices quadrupled in the 1970s oil crisis, the rate of energy productivity improvement rose over tenfold among (mostly oil-importing) OECD countries, from 0.2% to 2.1%.6

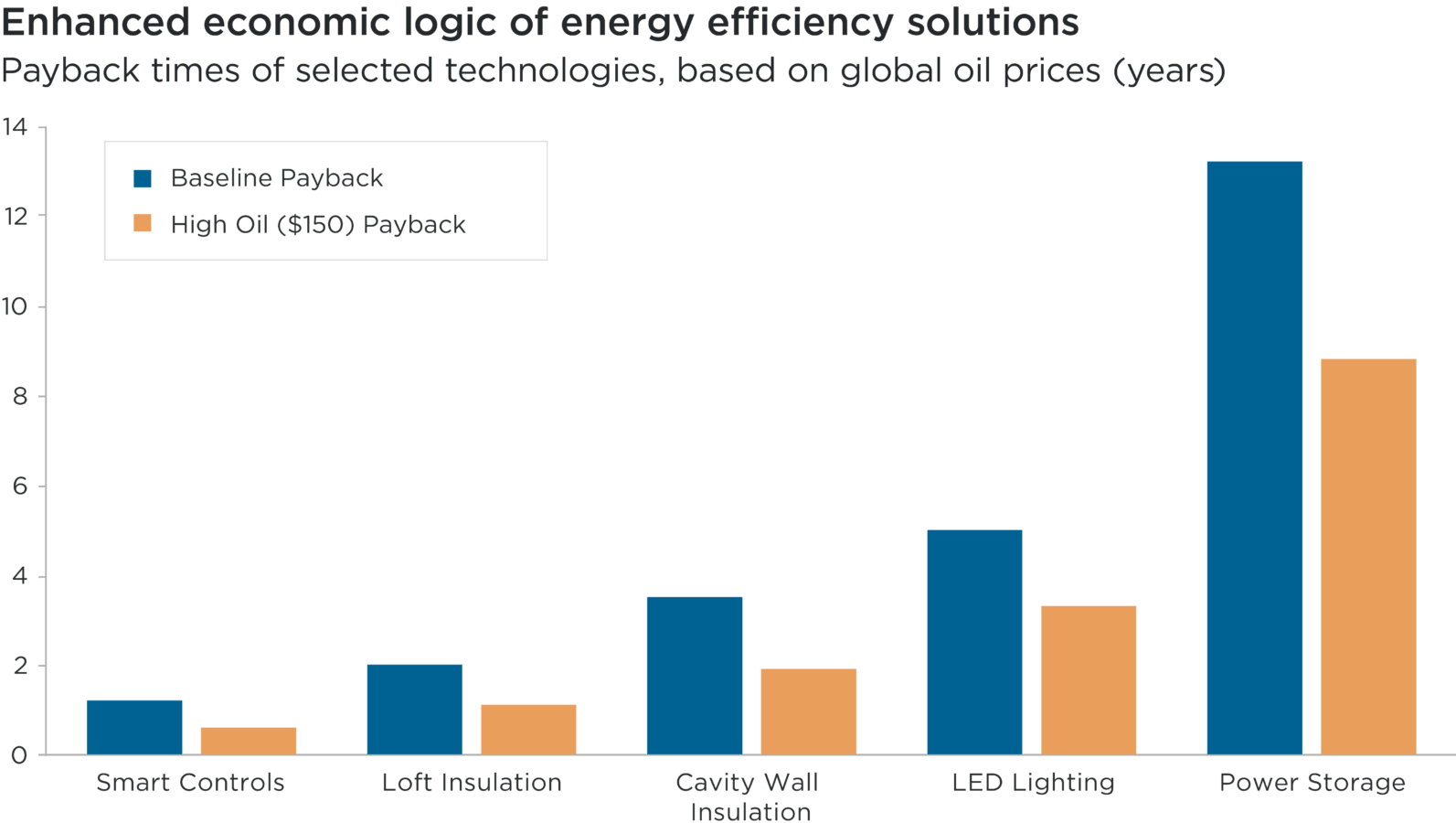

Illustrative analysis, based on UK figures and the assumption of a 50% jump in electricity prices, shows that the costs of adopting certain technologies can be recouped significantly faster when bills rise sharply (see chart below).

For energy users, lowering the cost of energy relative to total expenditure – whether as a household or a business – reduces vulnerability to external price shocks. The heat pump which brings peace of mind to a homeowner can do the same for a chief financial officer.

Source: Impax analysis, April 2026, based on a set of assumptions about the UK energy market and data from the House of Commons Library (2026) the Office for Budget Responsibility (2022), Ofgem (2026) and Capital Economics (2026).7 ‘Baseline’ calculations were based on UK energy prices as at April 2026, specifically the Ofgem price cap levels of 24.7p/kWh for electricity and 5.7p/kWh for gas.

Subhead: Payback times of selected technologies, based on global oil prices (years)

Overview: This bar chart shows the respective payback periods for selected energy management and efficiency technologies, based on baseline estimates for the UK in April 2026 and under a ‘high oil’ price scenario in which global oil prices reach US$150 a barrel.

Overall, this chart illustrates how higher oil prices can significantly shorten the payback periods for energy management and efficiency technologies, improving returns on investment for energy users who adopt them under these conditions.

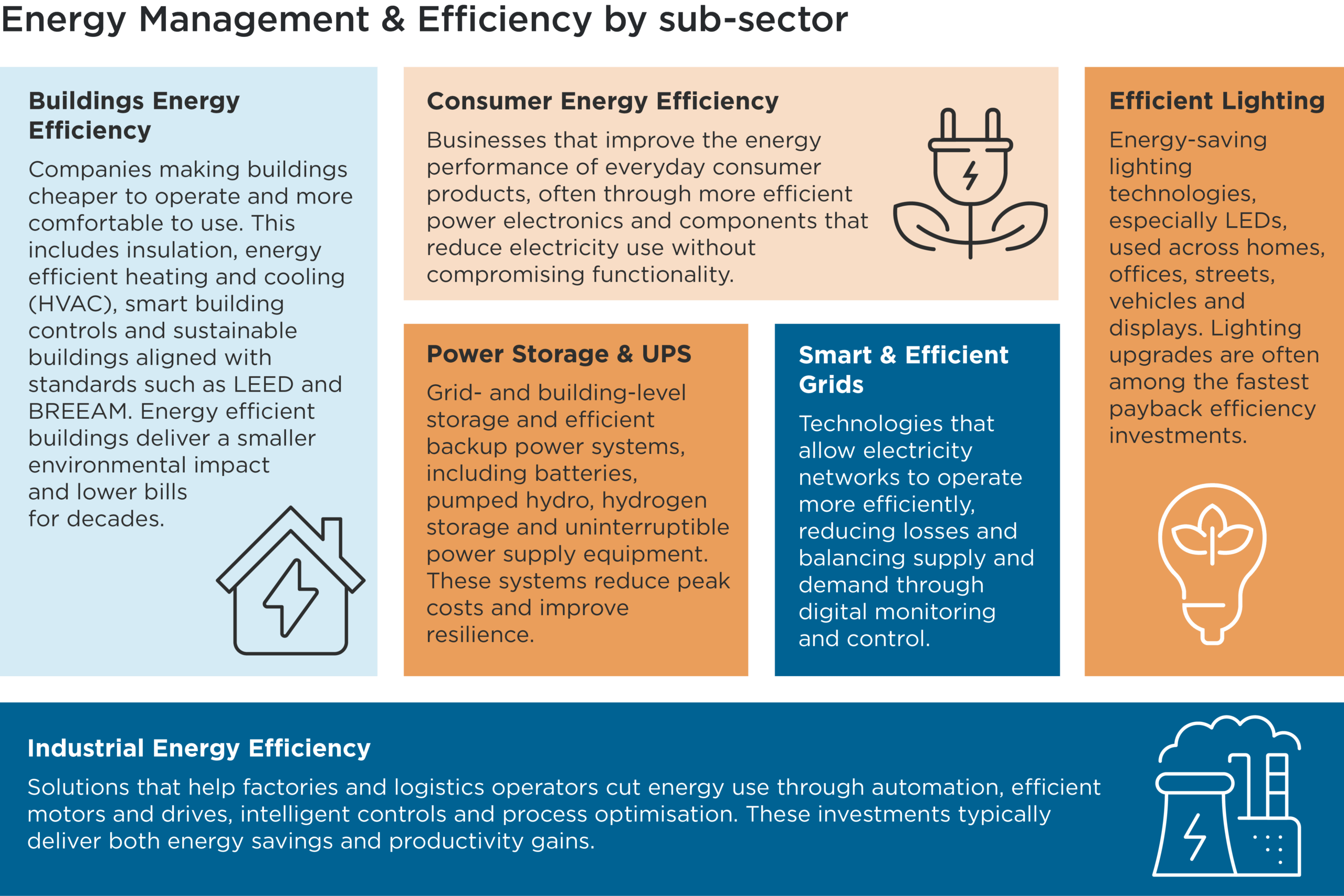

A breadth of environmental technologies

Within our Environmental Markets taxonomy, the Energy Management & Efficiency sector highlights products and services that help customers use less energy. Rather than focusing on a specific industrial sector or technology, the classification is sub-divided into six sub-sectors (below) where energy savings are measurable and repeatable.

Source: Impax, April 2026

Solutions need to demonstrate clear savings

Those companies that look best positioned in the context of elevated energy prices typically deliver clear, measurable energy savings for their customers and possess pricing power rooted in differentiated technology or regulatory systems.

They will also typically be beneficiaries of efficiency-driven capital expenditure (capex). Additionally, those that have established distribution capacity have the potential to capture volume growth at a time when returns on investment in energy efficiency are elevated. Three areas stand out in the current context.

First, smart energy management solutions. German-listed Siemens is an industrial technology conglomerate which provides building automation systems, HVAC controls and energy management software through its Smart Infrastructure division. These enable customers to optimise energy use and quantify operational savings in real time.

Second, products that directly reduce heating and cooling-related energy consumption. Irish-listed Kingspan is a manufacturer of high-performance insulation products that are designed to meet tightening energy efficiency requirements within government-mandated building regulations.

Third, heating, ventilation and air conditioning (HVAC) solutions. US-listed Carrier’s portfolio of products includes heat pumps and advanced building controls, which enable customers to reduce energy consumption, lower operational costs and enhance performance even as energy prices rise.

Pricing power remains paramount

Not all energy‑efficiency companies benefit from higher energy prices, however. Those that struggle typically share several structural vulnerabilities, including:

- Long or uncertain customer payback periods that remain uncompelling, even at elevated energy costs

- Exposure to discretionary consumer spending, rather than mandated commercial or industrial efficiency capex

- Energy-intensive manufacturing processes that face immediate margin compression on raw materials (especially the likes of plastics and steel, whose costs fluctuate with energy prices), production, and logistics – and particularly where companies do not have long-term hedges in place

- Commoditised products with limited pricing power to offset cost inflation

- Dependence on temporary subsidies that may be withdrawn once prices normalise or fiscal constraints tighten

These characteristics combine such that cost pressures hit immediately while any demand benefits lag. Companies without the necessary pricing power to offset these costs can therefore face an indeterminate period of margin erosion.

One sub-sector which looks more vulnerable in this context is efficient lighting. Production and testing are energy-intensive processes, yet the industry itself has low barriers to entry. LED technology is mature and component sourcing is commoditised, with particular dominance among lower-cost Asian manufacturers. The result is a crowded, competitive market with little room for differentiation. In this environment, sustained energy price inflation squeezes margins from both ends, raising input costs just as manufacturers compete on price to retain volume.

A moment of asymmetric opportunity

At a time of acute geopolitical uncertainty, consumers and businesses alike face added financial incentives to embrace technologies that help increase their resilience to elevated and volatile global energy prices. In many cases, the adoption of energy-saving products and services is likely to receive government support.

Higher energy prices create asymmetric opportunities across energy management and efficiency stocks, though. We believe energy management and efficiency stocks that can ably demonstrate clear cost savings to their clients, and meet rising demand within their operations and supply chains, look well positioned in this context. Those that are more exposed to discretionary spending and energy-intensive production face persistent headwinds, regardless of broader sector optimism.

Stock pickers who can distinguish between the long-term ‘winners’ and ‘losers’ of this latest energy shock will, in our view, be well placed to target outperformance.

1 ICE Endex Dutch TTF Natural Gas Futures Contract. Bloomberg, as at 15 April 2026

2 German Power Baseload Forward Year 1. Bloomberg, as at 15 April 2026

3 Brent Crude Oil futures. Bloomberg, as at 15 April 2026

4 IEA, February 2026: Electricity 2026

5 European Investment Bank, 2024: Invested in Renewables – The Only Way Forward

6 The Electrotech Revolution, April 2026: The New Twin Fossil Shock

7 House of Commons Library, February 2026: Gas and electricity prices during the ‘energy crisis’ and beyond

Office for Budget Responsibility, 2022: The changing impact of fossil fuel shocks on the UK economy

Capital Economics, March 2026: Scenarios for the Iran war & the macro impact

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point, and Impax Asset Management shall not be obligated to provide any notice. Forward-looking statements or forecasts herein are subject to known and unknown risks and uncertainties including inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. While Impax Asset Management has made reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.