United States

United StatesMake no mistake, the scale of investment required to build out AI-related infrastructure is vast.

Capital expenditure (capex) by the largest data centre operators – namely Amazon, Google, Meta, Microsoft and Oracle – is projected to rise this year to almost US$700bn.1 Increasingly, these investment grade ‘hyperscalers’ are drawing on credit markets to finance infrastructure expansion.2

AI-related financing within the high yield space remains comparatively limited, though, creating a notable supply divergence across credit quality segments. As at 5 March 2026, only 10 issuers had raised a total of US$26bn, representing less than 2% of the global high yield market.3

Nonetheless, mispriced risk has given rise to selective opportunities in this space, especially among data centre infrastructure issuers. ‘Neo cloud’ and AI model issuances have been fewer and more volatile.

So far, elevated supply of AI-related debt has not meaningfully disrupted spreads across either investment grade or high yield. Questions remain, though, about the longer-term impact of rising issuance – and the economics of issuers – as financing continues to scale.

Playing the AI theme via data centre issuances

Within high yield, issuances tied directly to data centre infrastructure and related power solutions have been strongly supported. Investors have been attracted by several factors: fully contracted revenue visibility, high quality tenants, structural protections embedded within special-purpose vehicles, lease backstops and/or execution support, and amortisation features.

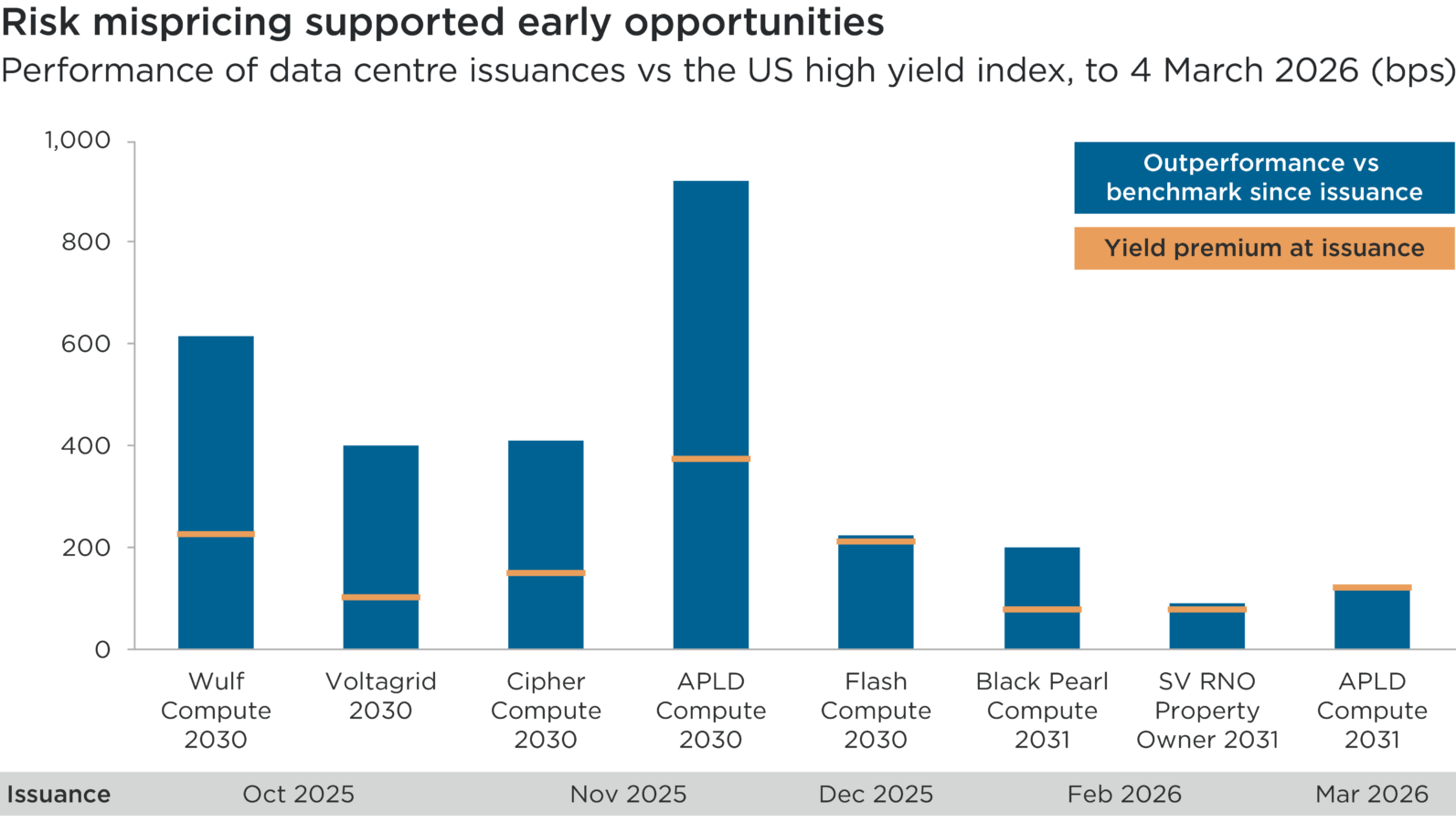

Yet despite perceived credit strength, relevant bonds issued between October 2025 and 5 March 2026 offered a yield premium that averaged 180 basis points (bps).4 Unsurprisingly, they have since significantly outperformed the overall high yield market – by an average of roughly 462bps, as at 4 March (see chart below).5

Structural demand for compute capacity continues to underpin the performance of these bonds. Prospective excess returns are moderating, however, as new-issue concessions have narrowed amid strong investor demand and rising comfort. In effect, infrastructure-backed AI financing has thus far behaved like a traditional asset-supported credit story, anchored by contracts, collateral and visibility of cash flows.

Past performance is not indicative of future returns.

For information purposes only. Not a recommendation to buy or sell any security. High‑yield/data‑centre exposures may be volatile and subject to credit, sector concentration, liquidity, interest‑rate and refinancing risks. You may not get back the amount invested.

Based on Impax analysis of Bloomberg data and underlying exposures of high yield issuances, as at 5 March 2026.

‘Outperformance vs benchmark since issuance’ represents the combined income and price returns of each respective bond from its pricing date to 4 March 2026, minus returns of the benchmark ICE BofA US High Yield Index over the same period. ‘Yield premium at issuance’ represents the difference between the coupon of each respective bond issued and the average yield of its respective five-year rating index on day of pricing.

Indices are unmanaged and not available for direct investment.

Subhead: Performance of data centre issuances vs the US high yield index, to 4 March 2026 (bps)

Overview: This bar chart compares the total return performance of high yield data centre issuances and their yield premiums at issuance, between October and early March 2026. The blue bars illustrate each respective bond’s relative performance, in terms of total returns, since issuance relative to the overall US high yield market (as measured by the ICE BofA US High Yield Index). The orange lines reflect each bond’s respective yield premium at issuance. Both metrics are in basis points (or bps).

Overall, this chart highlights how recent data centre issuances in the high yield universe have performed very strongly, relative to the overall US high yield market, having been issued at meaningful yield premiums. Yield premiums have tightened on more recent issuances during the period.

‘Neo cloud’ and AI model issuances

Beyond data centre issuances, there are two more limited avenues for high yield investors to gain exposure to the AI theme.

The first are vertically integrated ‘neo-cloud’ platforms: a new generation of AI-focused cloud providers that specialise in supplying AI developers with high-performance, on-demand GPU compute capacity. Their business models are highly capital-intensive given substantial upfront investment in data centres and specialised hardware.

While long-term contractual agreements provide revenue visibility, concentrated customer bases can be viewed as both a strength and risk. Key questions for credit investors evaluating neo-cloud structures also include capital market dependence, technology-cycle risk and the sustainability of long-duration growth assumptions.

Uncertainty regarding their perceived resilience is reflected in the early performance of bonds issued by CoreWeave, the only high yield neo-cloud issuer to date. Since their issuances in mid-2025, the US company’s bonds have experienced episodic drawdowns during periods of heightened scrutiny around AI valuations, funding durability and execution risk.6

The second alternative issuers are large language model (LLM) developers. Direct participation in public credit markets has been rare among LLM developers, with the notable exception of xAI. The developer of the Grok chatbot issued leveraged loans and high-yield bonds in June 2025 to finance data centre expansion and model development.7

Its bonds have exhibited much lower sensitivity to shifts in AI sentiment than observed in the neo-cloud issuances, in part because of the perception that opportunities are more protected at the heart of AI than in downstream infrastructure.

The performance of xAI’s bonds has also inevitably been esoteric, given an unusually large yield premium at issuance and investors’ track record of effectively underwriting long-duration businesses involving its founder, Elon Musk. Recent performance has been boosted by the announcement in February of xAI’s merger with SpaceX, the Musk-led developer of rockets and spacecraft, which has an established business model.

The evolution of xAI’s debt illustrates how changes in funding resilience can rapidly reshape perceived risk even before sustainable cash generation is established. LLM-focused issuers therefore present a distinct framework in which capital access, strategic sponsorship and execution against large-scale infrastructure plans matter more than conventional leverage metrics.

Investor selectivity remains paramount

For high yield investors, the next phase of the AI financing cycle is less about accessing the theme and more about identifying the capital structures most capable of converting technological momentum into resilient credit quality and compelling relative value.

Positively for issuers, structural demand for AI-related infrastructure appears durable. We also believe that rising capex requirements and potential for tighter regulatory constraints on the data centre build-out should provide partial technical support and help support credit stability.

Nonetheless, we expect that forward excess returns may moderate as spreads compress and new issuance scales. Prospective bond supply remains significant: it is estimated that upcoming projects will require finance totalling up to US$135bn.8 There is also a risk that underwriting standards may gradually soften as competition for capital intensifies and, based on previous experiences, the success of early transactions could encourage herd-like investor behaviour.

Broader secular risks are also likely to remain central to the investment narrative, particularly the realised return on capex, optimistic growth and revenue trajectories, and potential power constraints and/or supply-chain bottlenecks as AI infrastructure development accelerates.

There are also concerns about structural interdependence across the AI ecosystem. The perceived circularity between hardware supply, equity investment and end-customer demand may blur the distinction between durable end-market demand and financially supported growth, potentially amplifying downside risks if any participant reduces spending or if access to capital tightens.

Ultimately, long-term credit outcomes will depend on execution discipline, funding durability and the translation of AI adoption into sustainable cash flows. Against this backdrop, selectivity remains paramount.

Past performance is not indicative of future returns.

1 Futurum, February 2026: AI Capex 2026: The $690B Infrastructure Sprint

2 Murugaboopathy, P., 22 December 2025: AI spending spree drives global tech debt issuance to record high. Reuters

3 Impax analysis of Bloomberg data, 5 March 2026

4 Impax analysis of Bloomberg data, 5 March 2026. Yield premium is the difference between coupon of bond issued and average yield of the respective five-year rating index on day of pricing

5 Impax analysis of Bloomberg data, 5 March 2026. Performance versus return of ICE BofA US High Yield Index from date of pricing through 4 March 2026

6 Impax analysis of Bloomberg data, 5 March 2026. Coreweave 9.25% 2030 and Coreweave 9% 2031, as at 5 March 2026

7 x.AI LLC 12.5% 2030

8 Jefferies has tracked around 11 GW of project pipeline across various stages of development, equating to roughly US$135bn of capex spending, and between US$115bn and US$135bn of total funding needs

Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point, and Impax Asset Management shall not be obligated to provide any notice. Forward-looking statements or forecasts herein are subject to known and unknown risks and uncertainties including inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. . While Impax Asset Management has made reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.