United States

United StatesThe conflict in Iran may not be ‘over’, but credit spreads have largely unwound since their early-April dislocation. With this, the unresolved conversation about AI’s potential to disrupt software-as-a-service (SaaS) businesses – the so-called ‘SaaSpocalypse’ – is worth picking up.

Software stock valuations have bounced off their early 2026 lows, but debates around business model durability and terminal valuations remain unresolved. Share prices are arguably also being shielded by the broader risk-on mood in markets.

Within credit, the focus has been on software sector exposure, which is highest within private credit. While we remain constructive on certain pockets of the market, we are increasingly selective as a wave of refinancing looms and given uncertainties relating to the AI ‘supercycle’ – a structural force reshaping the fixed income market.

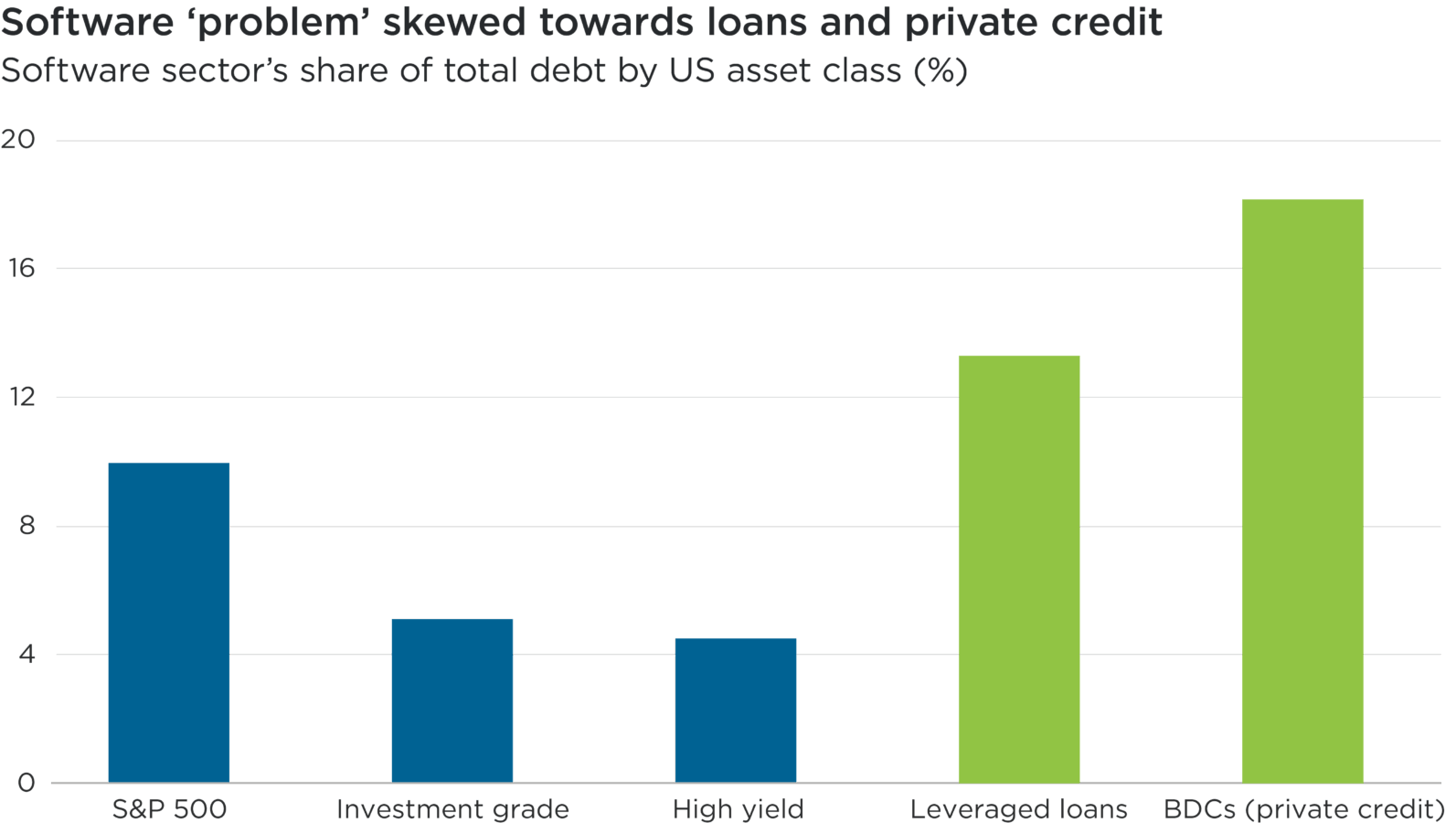

Contrasting asset class exposure to software

Within credit, software exposure is dramatically higher in private markets than in public markets. The sector only accounts for 4.5% of the US high yield universe; its share of the US leveraged loans market is three times greater (see chart below).1

The private credit market’s exposure to software is reported to be as much as 25%, although authoritative data is illusive.2 The sector makes up close to 20% of loans deployed by business development companies (BDCs), a type of private credit vehicle focused on US companies.

Source: JP Morgan data, March 2026. BDCs = business development companies

Subhead: Software sector’s share of total debt by US asset class (%)

Overview: This bar chart shows the software sector’s share, by percentage of outstanding debt, of five US asset classes: equities (as measured by the S&P 500), investment grade bonds, high yield bonds, leveraged loans and business development companies (BDCs), which are a type of private credit vehicle.

Overall, this chart illustrates the software sector comprises a much lower percentage of the high yield and investment grade bond markets, compared with those of leveraged loans and BDCs.

Pricing statistics in the US leveraged loan market provide some context for concern. Roughly half of software loans are rated ‘B-’ or lower, making software the single largest sector in the ‘B-’ bucket, and, as of early February, roughly 20% of the software loan universe was trading below 80 cents in the dollar – typically a sign of distress – up from 12% at end-2025.3

In addition, approximately half of technology-related loan issuance since 2021 has been tied to sponsor-driven leveraged buyouts (LBOs), mergers and acquisitions (M&A), and dividend-recapitalisation activity, so future underwriting must examine sponsor incentives as much as borrower fundamentals.

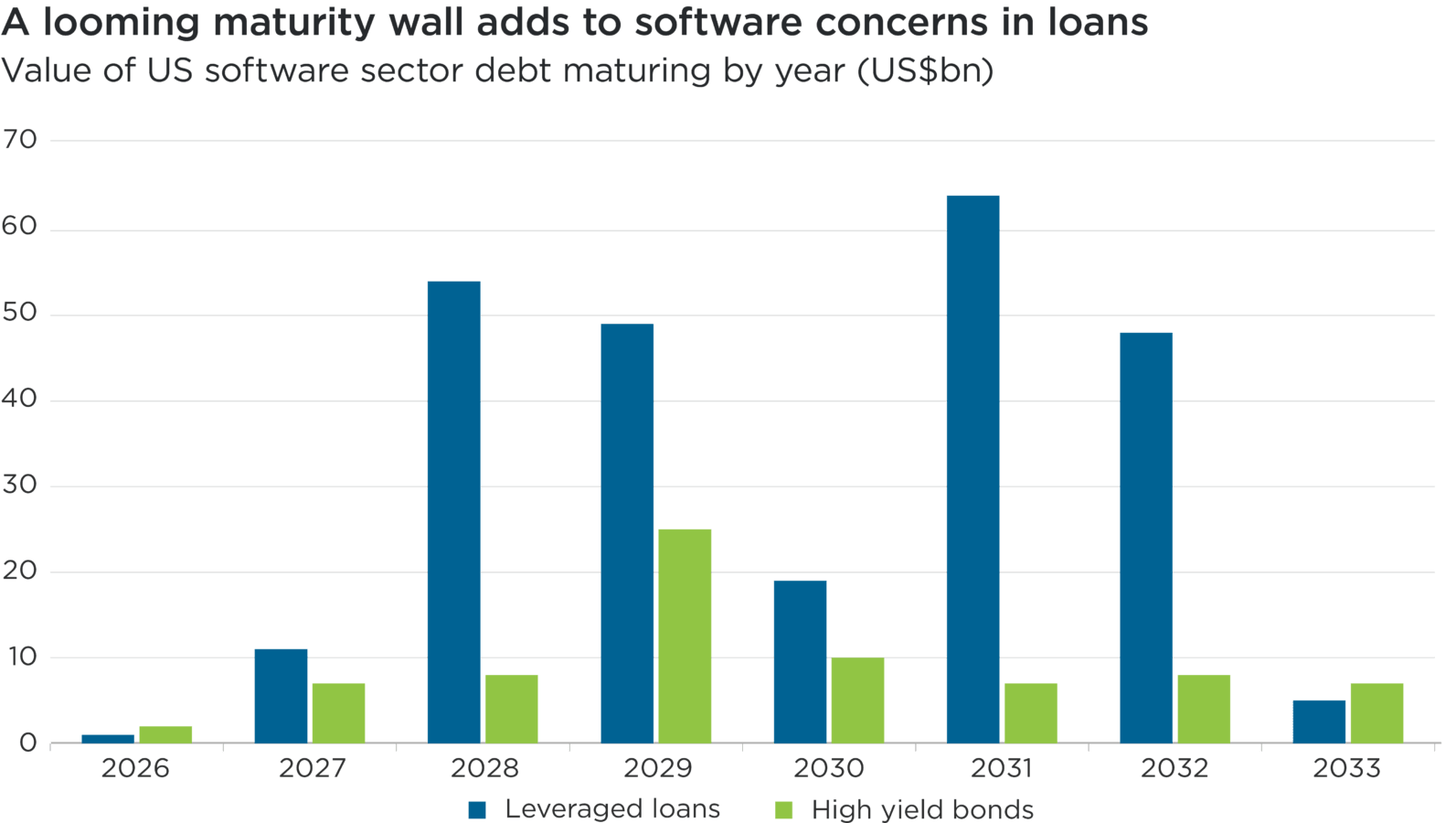

A glut of loans is maturing soon

While near-term cash flows are intact and it is difficult to see an imminent spike in defaults, the potential impacts of AI on business models cloud the future – especially when considered alongside a looming maturity wall that will require substantial refinancing.

More than US$100bn in US software-related leveraged loans mature in 2028 and 2029 (see chart below). Reports suggest that a substantial volume of private software loans and BDCs will be maturing then, too.4

Many of the loans that are coming due were underwritten at low coupons and elevated leverage, on the expectation of rising equity valuations. Refinancing these debts on comparable terms looks increasingly challenging.

It is unclear who is going to be willing to underwrite five-year forward risk – and at what price – given uncertainties over how AI will impact these businesses and especially with the concentrated maturity schedule.

Source: JP Morgan data, March 2026

Subhead: Value of US software sector debt maturing by year (US$bn)

Overview: This bar chart shows the value of software sector debt that is maturing, by year, through to 2033. It compares the value of maturing debt within the US high yield bond market and within leveraged loans.

Overall, this chart illustrates that a significantly greater value of software leveraged loans is maturing between 2028 and 2032, versus high yield debt issued by software companies.

Opportunities within AI infrastructure

High yield exposure to software may be the lowest among comparable credit markets, but this does not mean that we are complacent.

Given we cannot know how AI will evolve and disrupt the sector, we generally think it is prudent, as high yield investors, to avoid software issuances that do not offer compelling relative value. There are grounds for particular caution where leverage, sponsor incentives and unresolved terminal economics do not seem appropriately priced, given forward-looking risks. Instead, we continue to look for dislocated opportunities where bonds trade at a discount, but where issuer business models appear more resilient.

We perceive a strong opportunity set within AI infrastructure – specifically data centres and compute names that are beneficiaries of the ‘hyperscaler’ build-out. The credit enhancements across many of these special purpose vehicle structures behind these deals look fundamentally more attractive, in our view, than a SaaS leverage profile in an environment where compute and power demand still outweighs supply.

This notwithstanding, technical factors are softening. Recent issuance in this space has been heavy and structural protections for lenders (including loan-to-capital ratios and sponsor checks) have incrementally weakened. In addition, premiums have narrowed on more recent issues and we observe that they have not traded as strongly in the secondary market.

Grounds for caution

Against this backdrop, we remain constructive on the AI infrastructure layer but are increasingly selective, looking for individual entry points where the structure justifies the risks.

More broadly, we continue to believe that near-term results will be fine for most software-related names. As we look forward, however, it becomes difficult to know who the ‘losers’ from AI disruption will be, especially given the speed of technological evolution and the fast-approaching wall of maturing debt.

1 JP Morgan data, March 2026

2 S&P Global data as at December 2025, cited by Prime Buchholz, February 2026: Software Stress & AI Risk in Private Credit

3 Morgan Stanley, February 2026

4 S&P Global, March 2026: BDCs’ Exposure To Software Stays High, Steady

Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point, and Impax Asset Management shall not be obligated to provide any notice. Forward-looking statements or forecasts herein are subject to known and unknown risks and uncertainties including inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. . While Impax Asset Management has made reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.