United States

United StatesUS companies have virtually stopped issuing impact bonds. Amid waning investor interest and a hostile political climate, only a couple of sizeable labelled corporate bonds came to market in early 2025.

Yet the investment case for impact bonds remains fundamentally intact. It is our conviction that the dearth of new labelled corporate debt only amplifies the longstanding case for looking at non-labelled equivalents in pursuit of risk-adjusted returns.

* 2025 Q1 data to 27 March 2025

Source: Bloomberg, 27 March 2025, based on Bank of America Merrill Lynch data. Issuances exceeding US$250mn.

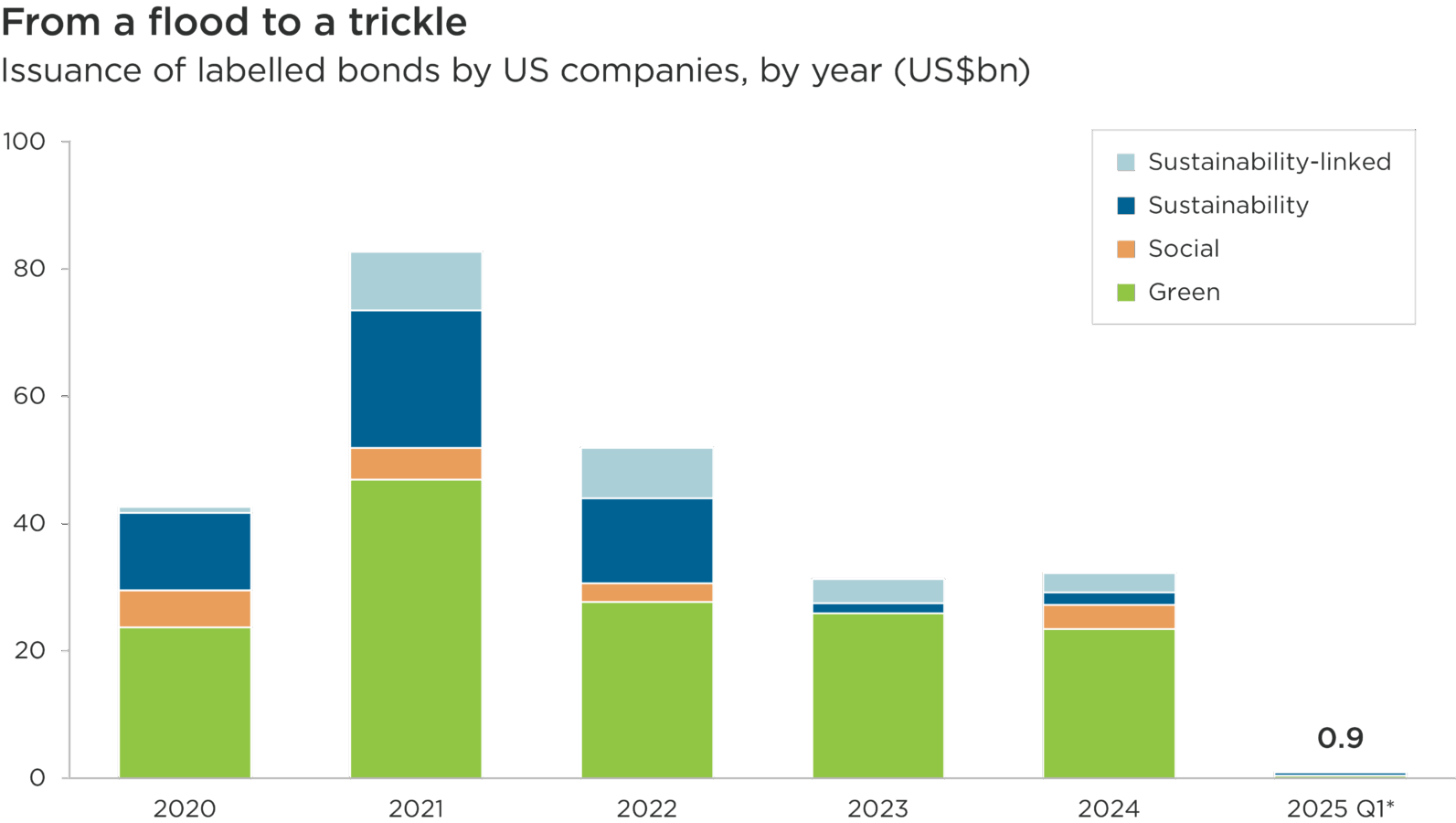

Subhead: Issuance of labelled bonds by US companies, by year (US$bn)

Overview: This bar shows the combined value of new labelled bonds issued by US companies in each year, 2020 to 2024, and in the first three months of 2025. The data shows the breakdown, by year, of issuances according to type of label: green, social, sustainability and sustainability-linked.

Overall, this chart illustrates the sharp downward trend of labelled bond issuance by US companies. Since peaking in 2021, the combined value of labelled issuances almost halved in 2022 and again in 2023, before stabilising in 2024. Issuances in the first three months of 2025 have been negligible, however.

New issuances have dried up

The US corporate sustainable bond market has ground to a halt in 2025. Only two such bonds (of at least US$250mn) were issued in the first quarter: a US$350mn green bond from Oglethorpe Power and a US$500mn sustainability bond from Starwood Properties. For context, in the first quarters of 2024 and 2023, respectively, labelled bond issuances by US companies totaled US$9.7bn and US$12.1bn.1

From our conversations with issuers and bankers, there are three primary reasons for the sharp decline in US corporate sustainable bond issuance.

First, labelled debt is relatively expensive to issue. Costs can include consultant and lawyer fees, and setting up reporting requirements can incur operational expenses. There was some belief that these costs could be mitigated by the emergence of a ‘greenium’ – a premium paid for labelled bonds over non-labelled equivalents in the form of lower yields. The research on greeniums is mixed, however, and is, at best, very small for US corporate issuers.2

Second, issuers fundamentally feel no pressure from investors to issue labelled debt. In the recent past, investors encouraged issuers to do so, motivated by the potential benefits outlined below. That has changed: it is apparent from speaking with issuers that mainstream asset managers now have less focus and interest in this area.

Third, and related, is the unfavorable political climate. President Trump and the Republican administration has made clear their antipathy towards finance being mobilized in support of environmental and social objectives. Issuers and investment managers concerned about incurring political wrath by association with sustainable finance appear to be heeding the message.

The fundamental appeal of impact bonds

The collapse of issuance in the US has done nothing to undermine the investment case for green, social, sustainability and sustainability-linked debt, in our view.

Impact bonds can primarily offer three diverse qualities within portfolio allocation: diversification, stability and transparency.

First, diversification: impact bonds span multiple asset classes that are both within and outside of benchmark indices, with many being less correlated with traditional holdings. Additional diversification can support risk management within portfolios like large investment grade strategies.

Second, relative stability: the buy-and-hold nature of many sustainability-focused investors can lead to lower price volatility as these bonds often trade less frequently than conventional securities. Investors that engage in relatively small transactions can remain nimble, however; our team leverages specialized sell-side relationships that allow us to break up larger trades into more digestible sizes and provide sufficient liquidity.

Third, transparency: regular impact and allocation reporting gives us a window into companies’ sustainability profiles. In general, we think issuers that are paying attention to sustainability-related risks should better manage them over time, in turn reducing creditors’ exposure to possible defaults arising from these risks.

Looking ‘off label’ to navigate the drought

The collapse in new issuance highlights the limitations of focusing solely on labelled debt. The markets love labels, but we have long thought it important to evaluate non-labelled corporate impact bonds. While they typically require deeper analysis, they can provide broader investment opportunities.

Non-labelled corporate impact bonds often provide investors with the opportunity to invest in longer-dated maturities (more than 10 years) and larger deal sizes (more than US$750mn) compared to their labelled counterparts. Labelled bonds often have tenors of six to eight years as the maturity is intended to align with the life of the project being funded. Longer duration allows investors to potentially realize greater returns if the credit thesis plays out as intended.

To effectively evaluate and select non-labelled impact bonds, we employ a multi-faceted approach. This includes conducting thorough issuer-specific research to understand the environmental and social merits of each bond, assessing the impact of financed projects, and maintaining flexibility in labelling securitizations.

Ultimately, the global opportunity set for impact bond investment remains vast. Labelled bond issuance is still expected to reach approximately US$1tn in 2025 for the fifth consecutive year, demonstrating the resilience of the broader global market even as US corporate participation wanes.3

As the impact bond market continues to evolve, we believe that investment teams who allocate resources and expertise to carefully analyzing the financial merits and additionality of individual issuances will be well-positioned to generate both carefully considered impact and risk-adjusted returns.

1 Bloomberg, 27 March 2025, based on Bank of America Merrill Lynch data. Issuances valued at US$250mn or greater. 2025 data to 27 March 2025.

2 MSCI, 2024: Is Greenium Evaporating in USD Corporate Bonds?

3 S&P Global Ratings, February 2025: Sustainability Insights: Global Sustainable Bond Issuance To Hold Steady At $1 Trillion In 2025

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.