United States

United StatesSince the global financial crisis, banks in the US – as in Europe – have had their wings clipped by regulation and high capital requirements. Rock-bottom interest rates have further crimped returns on equity.

Almost two decades on, these headwinds are reversing. Deregulation, balance sheet strength and a higher-for-longer interest rate outlook now promise to usher in a period of renewed opportunity and consolidation within US banking.

We see dynamic regional banks, which remain central to enabling financial inclusion across the world’s largest economy, as among the prime beneficiaries of these tailwinds.

A sector finally out of the doghouse

Stringent regulatory frameworks like the Dodd-Frank Act and Basel III rules have imposed high balance sheet requirements and rigorous stress tests on US banks. Regulation has tied up capital and raised costs.

Regulatory headwinds are now reversing into strong tailwinds as the Trump Administration actively pursues financial sector deregulation. While public policy can quickly change, we observe four important steps that indicate the direction of travel so far in 2025.

First, US banks are no longer being punished for past misdemeanours. In June, the Federal Reserve lifted an asset cap imposed on Wells Fargo since 2018, following a major scandal involving fake customer accounts.1

Second, regulators are taking a more constructive stance towards consolidation in the highly fragmented US financial system. The swift approval of Capital One bank’s US$35bn acquisition of Discover this April, bringing together two of the US’ largest credit card lenders, sets the scene for more mergers and acquisitions (M&A) activity.2

Third, the Fed has proposed relaxing rules on how much capital banks must hold against relatively low-risk assets like US Treasuries. These changes could unlock up to US$6tn in additional balance sheet capacity, according to some estimates.3

Fourth, and related, are proposals to soften or remove artificial thresholds that trigger higher capital requirements as banks grow.

Source: Bloomberg data, 22 July 2025. End-year data. 2025 figures are consensus estimates.

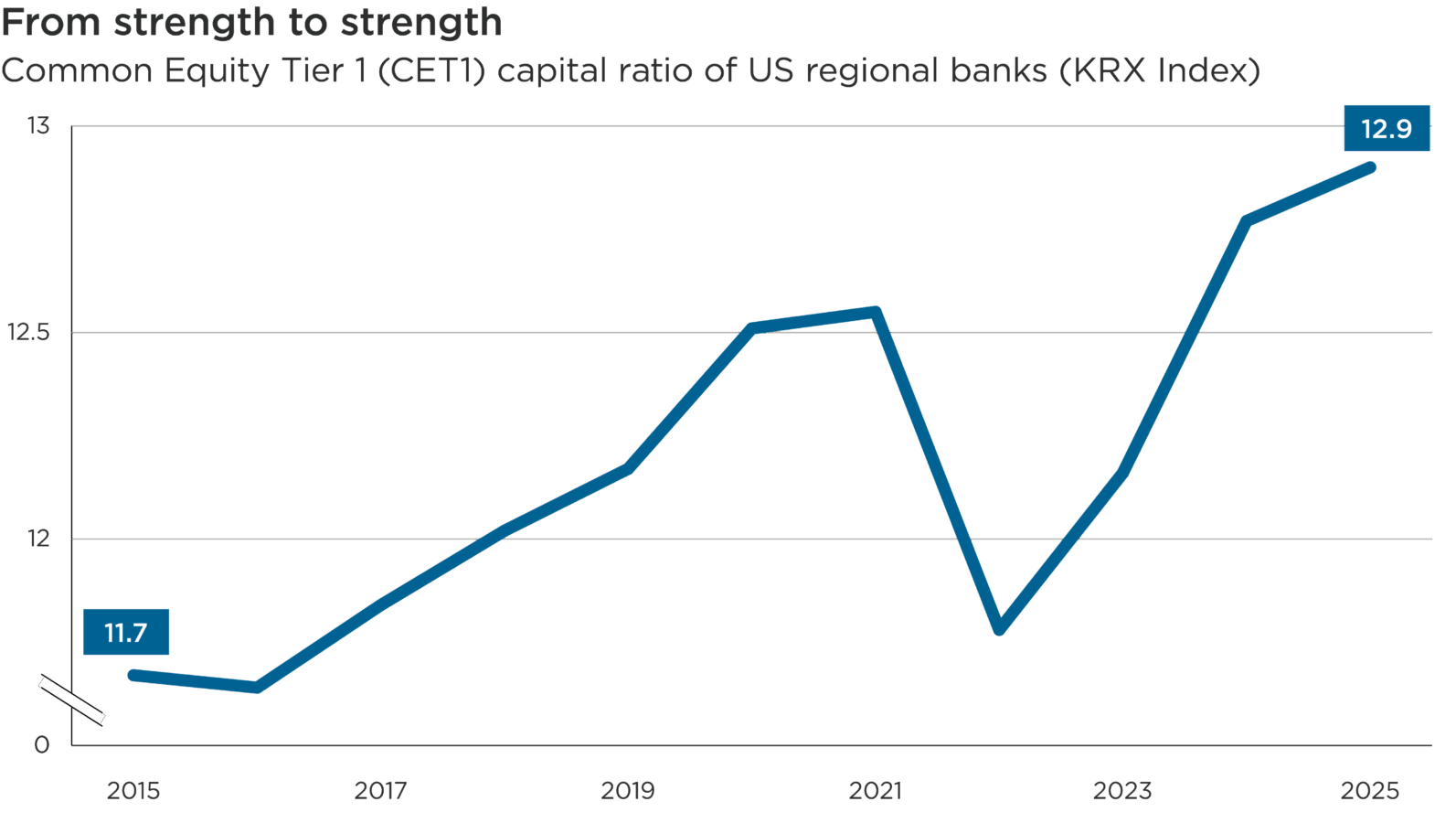

Subhead: Common Equity Tier 1 (CET1) capital ratios of US regional banks

Overview: This bar chart shows the Common Equity Tier 1 (CET1) capital ratios of US regional banks overall, as measured by the KRX Index, between 2015 and 2025.

Overall, this chart reveals a generally upward trend in the CET1 capital ratios of US regional banks over the past decade.

Balance sheet strength in a low-rate environment

Strictures placed on the sector have contributed to robust balance sheets. Capital buffers are close to all-time highs: Common Equity Tier 1 (CET-1) ratios, which compare a bank’s liquid capital and risk-weighted assets, have continued to rise since the pandemic.4 Asset quality also remains strong: although the percentage of loans in arrears has risen, it remains below pre-pandemic levels.5

The return to more historically ‘normal’ US interest rates since 2022 has meanwhile led to higher returns on assets and net interest margins – the difference between what interest banks earn on assets, like loans, and what interest they pay on liabilities, like deposits.6

Banking margins should be supported by higher-for-longer interest rates: expectations of material rate cuts in the US have sharply moderated since the 2024 election ushered in a more expansionist fiscal stance. Monetary policy can quickly change in response to economic conditions, but most Federal Open Market Committee members now expect US base interest rates to remain above 3% in 2027.7

In this environment, and as regulatory hurdles are removed, US banks should be able to deploy their surplus capital more efficiently to drive shareholder returns. We expect a resurgence in M&A activity: while the pace of consolidation has slowed in the past five years, the number of US banks has fallen from roughly 14,500 in the early 1980s to a little over 4,000.8 Economies of scale in the highly regulated digital banking era underscore the logic of further consolidation.

Why regional banks look primed to benefit

In our view, leading regional and community banks are well placed to capitalise on these tailwinds. Smaller institutions remain highly relevant in a competitive market, controlling around 28% of US banking assets.9 This reflects success in nurturing deep, long-term ties with individuals and small businesses.

We see particular investment opportunities in regional banks that operate in dynamic economies in the South and Southeast – home to seven of the 10 fastest-growing US states – as loan and deposit growth should grow faster than the national average.10

Cullen Frost is the sixth-largest bank by assets in fast-growing Texas, the second-largest state economy in the US.11 It has been the highest-rated retail bank for 16 years.12 Pinnacle Financial, the largest bank in Nashville – one of the fastest-growing US cities – meanwhile continues to open branches to serve its expanding customer base across Tennessee, the Carolinas and Virginia. In July, Pinnacle announced a merger with another leading bank in the southeast, Synovus Financial, whose approval would reinforce the deregulation trend.13

We also perceive opportunities among regional banks whose corporate turnarounds coincide with improving banking conditions. Citizens Financial, one of the largest banks by assets in New England, has been transformed since its spin-out from the Royal Bank of Scotland in 2014 and is now expanding in key markets.14

Recent Q2 results reported by US banks have painted an encouraging picture, with rising demand for loans, a steeper yield curve helping margins and a strong pipeline of capital markets activity, all coupled with a benign and improving credit environment. Regional bank valuations meanwhile significantly lag those of the overall US mid-cap market.15

Figures refer to the past. Past performance does not guarantee future results. Indices are unmanaged and it is not possible to invest directly in an index.

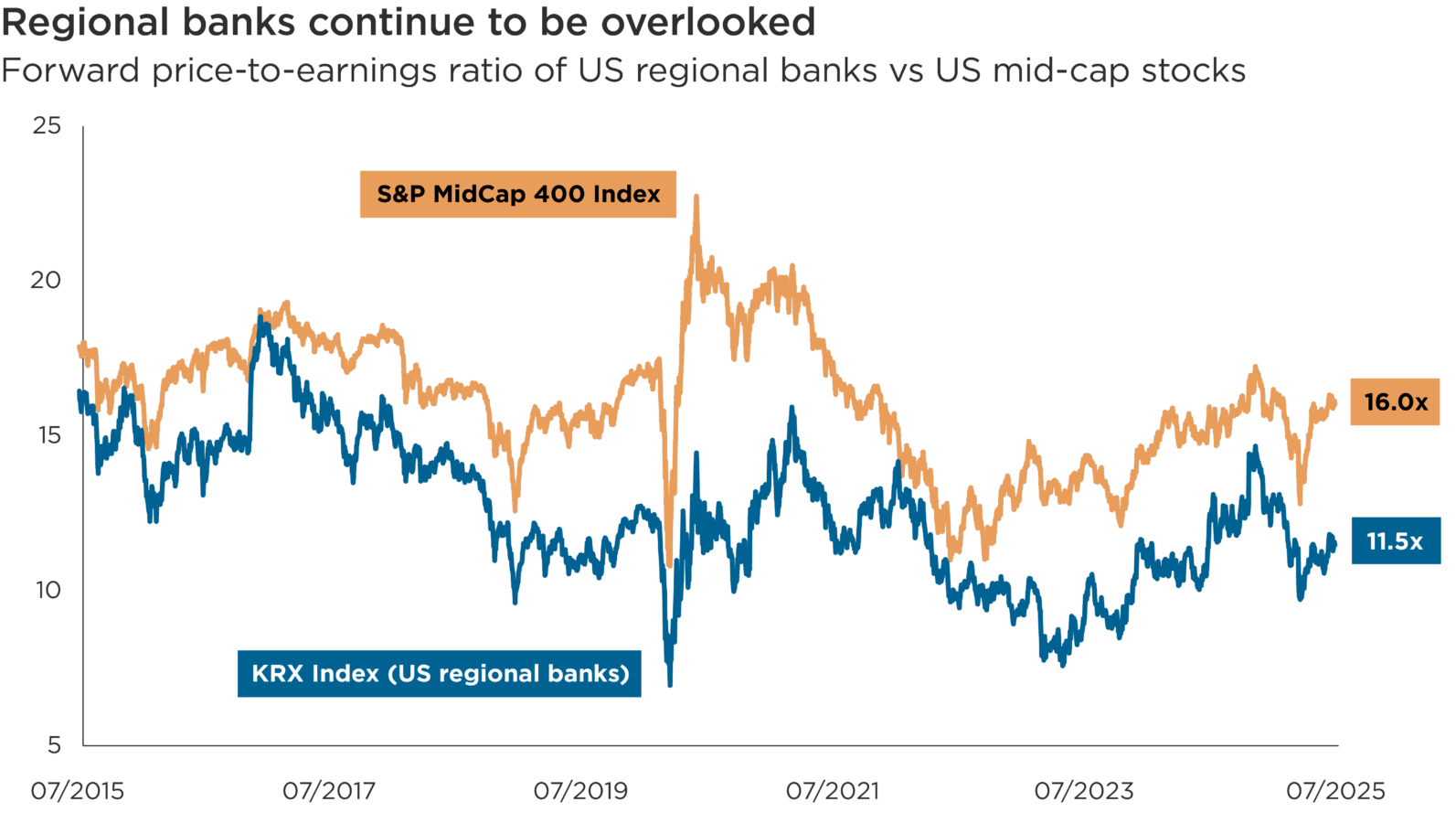

Source: Bloomberg data, 22 July 2025

Subhead: Forward price-to-earnings ratio of US regional banks versus US mid-cap stocks

Overview: This line chart compares the forward price-to-earnings (PE) ratio of US regional banks overall, as measured by the KRX Index, versus that of US mid-cap stocks, as measured by the S&P MidCap 400 Index, between July 2015 and July 2025.

Overall, this chart shows how relative valuations between US regional banks and the overall US mid-cap market have diverged over the past decade. The forward PE ratio of US regional banks stood at 11.5 times projected earnings, as at 22 July 2025, compared to 16.0 times for the overall US mid-cap market.

Opportunities in broadening economic inclusion

Access to finance is a key ingredient for economic and social mobility. Ultimately, by enabling financial inclusion, banks can help unlock and underpin a self-reinforcing cycle of opportunity: a more prosperous customer base should support growing demand for financial services.

With their local expertise and focus on customer relationships, US regional banks can play a key enabling role within communities. As the sector enters a period of deregulation with strong balance sheets, and supported by constructive monetary conditions, we see conditions in which regional bank shareholders should benefit from improved returns and takeover activity.

1 Bloomberg, 3 June 2025: How Wells Fargo Emerged From Years of Regulatory Sanctions

2 Chu, A. & Franklin, J., 18 April 2025: Capital One’s $35.5bn takeover of Discover Financial approved by US. Financial Times

3 Saini, M., 26 June 2025: Wall Street forecasts windfall for big US banks from Fed plan to ease leverage rule. Reuters

4 Bloomberg data, 22 July 2025

5 Federal Deposit Insurance Corporation, May 2025: FDIC Quarterly Banking Profile First Quarter 2025

6 Federal Deposit Insurance Corporation, May 2025: FDIC Quarterly Banking Profile First Quarter 2025

7 Federal Reserve data, as at June 2025. Jones, C., 18 June 2025, Federal Reserve cuts outlook for US economy but holds interest rates steady. Financial Times

8 Federal Deposit Insurance Corporation, 2023

9 USA Facts, 2023: How strong are regional and community banks in the US?

10 U.S. Bureau of Economic Analysis, June 2025. Real GDP growth by state: First quarter 2025

11 Federal Deposit Insurance Corporation, as at 30 June 2024

12 JD Power, 2025: US Retail Banking Satisfaction Study

13 Pinnacle Financial, 24 July 2025: Pinnacle Financial Partners and Synovus Announce Merger

14 Citizens Financial Group, October 2024: 2024 Annual Review

15 Bloomberg data, 22 July 2025. As measured by forward price-to-earnings ratios

This material contains past performance information. Past performance does not guarantee future results.

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.