United States

United StatesTechnological innovation and the transition to a more sustainable economy are prompting a vivid reimagination of how people and goods can move from A to B.

Innovations in the sharing economy promise to disrupt established models for personal mobility. The value of the shared mobility market, which includes ride-hailing and vehicle rental services that offer alternatives to car ownership, now exceeds US$60 billion across China, Europe and the US, according to McKinsey.1 However, most business models are currently loss-making.

Promising alternatives to fossil fuels, meanwhile, have the potential to align the transport sector, which accounts for 24% of global CO2 emissions from fuel combustion, with net-zero goals.2 The hard-to-abate shipping sector could cut emissions by using ammonia produced using renewable electricity. There is also great potential for sustainably derived hydrogen to replace diesel in powering trucks. But these future fuels remain highly speculative, with technological and infrastructure challenges to overcome.

In one area of the transport sector, though, a revolution based on proven technology is well underway and demonstrates how clean transport can rapidly grow. The accelerating shift to electric vehicles (EVs) is also creating significant opportunities for long-term investors.

Personal mobility: from high octane to high voltage

The electrification of light vehicles is arguably the most significant change in the car market since the advent of mass production, which drove the cost of car ownership down to more affordable levels a century ago.

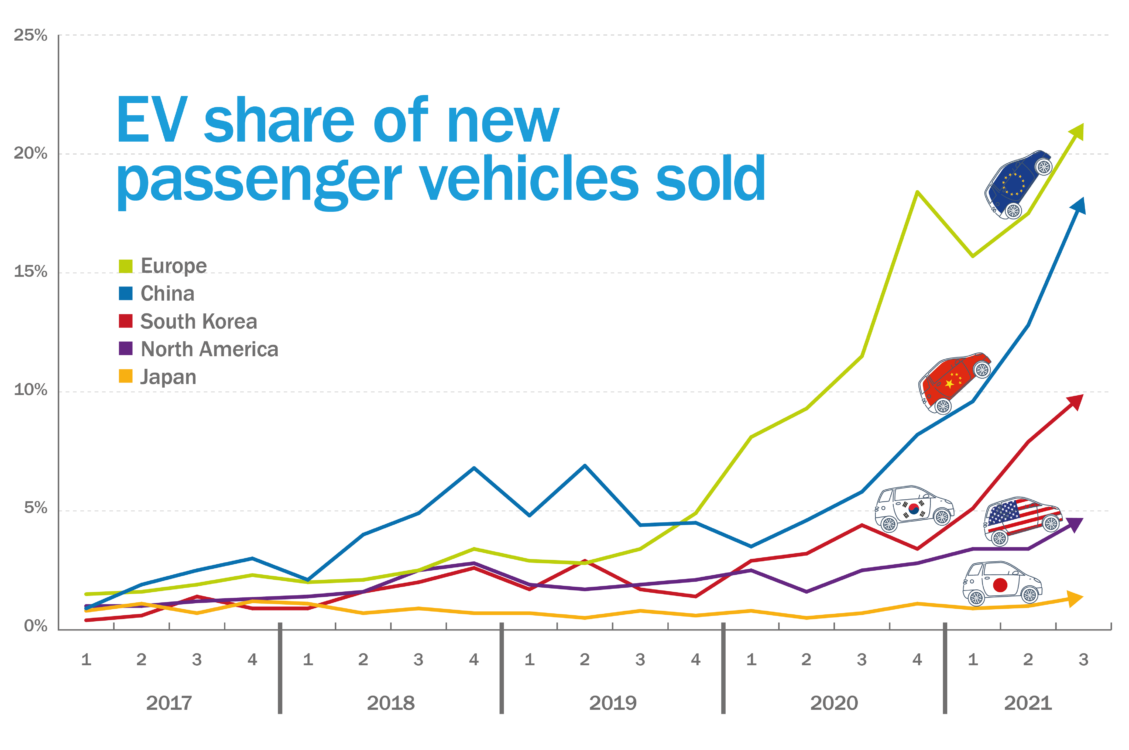

It is estimated that more than 6.3 million passenger EVs were sold in 2021 — almost twice the 2020 total.3 While this remains a low single-digit percentage of new car sales worldwide, electric models have gained significant market share in many developed markets. Across Europe, EVs had captured 21% of new car sales by Q3 2021. In Norway, generous incentives drove EVs to a record 65% market share in 2021.4

Note: EV sales include battery electric vehicle (BEV) and plug-in hybrid electric vehicle (PHEV) sales.

Europe data includes EU27 countries plus Norway, Switzerland, Iceland and the UK.

North America data includes Canada and the US. China data excludes low-speed EV sales.

Four broad factors have catalyzed the EV transition: evolving consumer preferences, battery technology, incumbent adoption and policy decisions.

First, car buyers have cooled on the internal combustion engine (ICE) as society has become more concerned about climate change and pollution. The 2015 “Dieselgate” scandal, when Volkswagen was found to have cheated emissions tests, has had a lasting imprint on consumers (as well as regulators and carmakers themselves). Diesel’s share of new sales has fallen precipitously, accounting for only 5% of UK car sales in January 2022, down from 48% in 2016.5 Meanwhile, the appeal of EVs has grown following the emergence of Tesla as a premium all-electric alternative. Demand growth also comes from corporate buyers looking to decarbonize their fleets.

Second, advances in battery technology have gone a long way to addressing the range anxiety cited by many hesitant car owners. The Tesla Model S can drive up to 412 miles on one charge. Critically, batteries have also become much cheaper as production capacity — 70% of which is in China — has swiftly ramped up.6 Lithium-ion battery prices fell by 89% from 2010 to 2020, helping cut the cost of new EVs.7

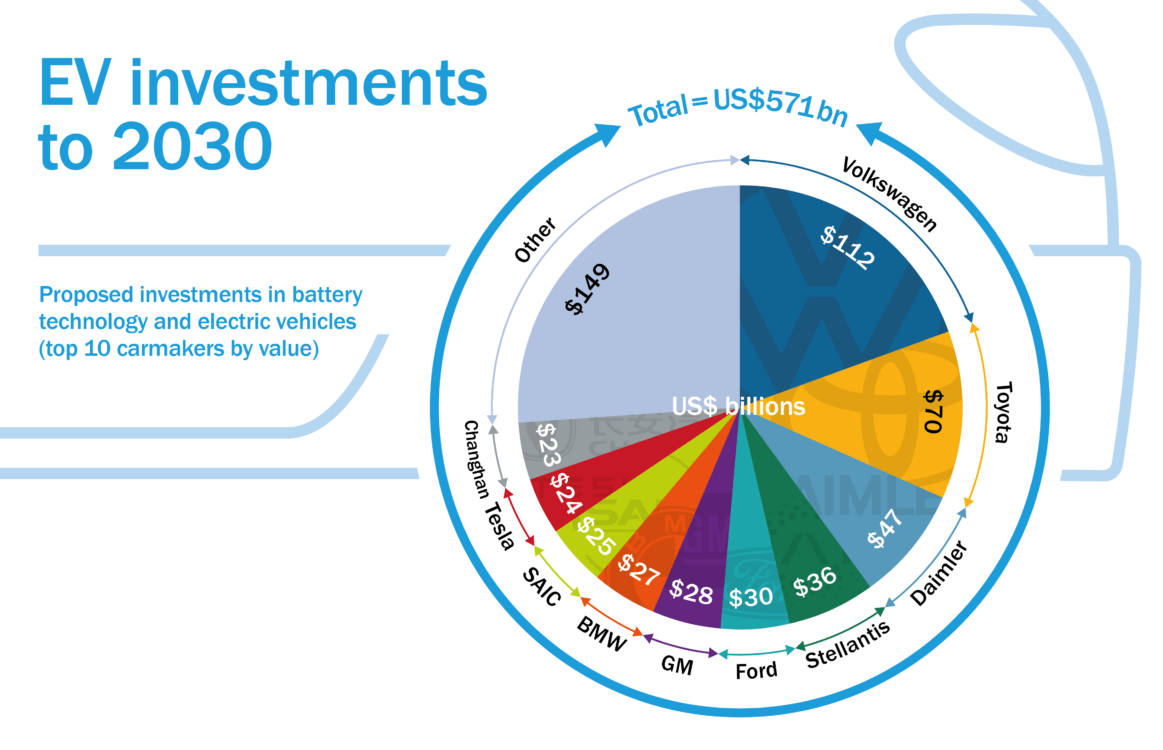

Third, incumbent carmakers have embraced the EV drivetrain. Their commitment is demonstrated by the growing choice of models arriving on forecourts, the result of vast investment. Two of the world’s largest carmakers, Volkswagen and Toyota, recently announced plans to invest roughly US$100 billion and US$70 billion respectively into developing new EV models this decade.8

Updated by Impax to reflect Toyota announcement in Dec 2021.

Finally, policymakers have pushed the accelerator to encourage the transition away from ICEs. As well as fiscal incentives for EV buyers, many governments have subsidized the roll-out of public charging infrastructure to remove barriers to EV take-up. Driven by air quality concerns, cities from London to Beijing have introduced low emission zones and privileges for EV drivers. Most importantly, national commitments have been made to end the sale of ICE cars and vans. At the COP26 climate summit in 2021, more than 100 countries pledged to do so by 2040 or earlier, and by 2035 in developed markets. This reinforces a clear direction of travel.

Investment opportunities in EVs: looking under the bonnet

The most obvious components for powering the EV transition, namely batteries and charge points, are not necessarily the most attractive areas for investors. They are not only capital-intensive industries, but also increasingly commoditized products — the reason cited when UK company Johnson Matthey pulled the plug on its EV battery business in November 2021.9 Given the economies of scale involved, we expect only the most efficient battery-makers to thrive. Government intervention may also distort the market.

Instead, we believe the most promising opportunities lie in technologies that can enable trends within the EV transition, including that toward autonomous vehicles. The likes of Motional — a joint venture between mobility technology company Aptiv and Hyundai — are trialing robo-taxis in small areas like Las Vegas. The enabling technologies that could propel autonomous EVs into the mainstream are advancing and are increasingly embedded in today’s vehicles.

Electrification has also allowed a reimagination of vehicle architecture. Modern EVs have a software-controlled central nervous system that connects their moving parts to digital eyes and ears, in the form of cameras, radar sensors and lidar sensors. These sophisticated components, and the software that translates their inputs into self-driving capabilities, underpin advanced driver-assistance systems that can offer varying degrees of autonomy, from warning of lane departures to self-driving under certain conditions.

A second promising area lies in connectivity technology, into which at least US$60 billion was invested in the decade to 2020.10 This includes vehicle-to-infrastructure communication, connecting vehicles to traffic signals and variable speed limits so they can respond autonomously; vehicle-to-vehicle communication, enabling vehicles sharing a road space to exchange data on their location, direction and speed; and vehicle-to-network communication, connecting passenger devices to digital infrastructure so journey times can be spent more productively (or enjoyably).

Keeping vehicles firmly connected to the cloud clearly will be imperative as connectivity and autonomy advances, and carmakers are partnering with technology companies to ensure connections are robust and secure. Given the vulnerabilities associated with connected devices and public EV charging points, cybersecurity is a key concern. As well as incorporating more advanced protection systems in the design phase, software companies provide over-the-air updates and patches to EVs once vulnerabilities are detected.

We believe these enabling technologies stand to play central roles in the future of personal mobility over the decades ahead, irrespective of which branded badges adorn the cars we drive or are driven by.

1McKinsey Center for Future Mobility, February 2022

2IEA, 2020: Tracking Transport 2020

3Bloomberg NEF, 15 December 2021: 4Q 2021 Electrified Transport Market Outlook

4Bloomberg, 1 February 2022. EV Sales Hit Record in Norway With Fossil Engines Soon Gone

5Society of Motor Manufacturers and Traders, February 2022

6IEA, November 2021: Electric Vehicles

7Bloomberg NEF, 2021. Electric Vehicle Outlook 2021

8Bloomberg, 5 January 2022: Titans of Carmaking Are Plotting the Overthrow of Elon Musk

9Johnson Matthey, 11 November 2021

10McKinsey & Company, 14 April 2021. Mobility’s future: An investment reality check

IMPX-20220316-1021