United States

United StatesIncreased delinquencies, sponsor bankruptcies and rating agency downgrades among solar loan asset-backed securities (solar ABS) highlight the risks facing investors in an important area of the sustainability fixed income market.

Solar ABS scores highly on sustainability metrics and, following recent repricing, can offer attractive valuations relative to other securitised products.1 However, the prospects for the US residential solar industry have been clouded by higher interest rates and the proposed rollback of clean energy tax credits.2

While solar ABS can present attractive investment opportunities, investors need to carefully consider the risks. In the current context, having a thorough understanding of the credit quality and borrower behaviour of the underlying loans, the structural nuances of each transaction, and the financial strength of counterparties involved, is essential.

Challenges facing the sector

For fixed income investors, the fundamental appeal of solar ABS lies in their valuations (see chart below) and prime credit quality collateral pools.

By pooling loans taken out by homeowners to install residential solar systems, the ABS structure redistributes credit risk from a pool of illiquid loans to investors and often provides cheaper financing for solar issuers compared to other funding options. Access to financing has, in turn, helped spur the growth in solar loan originations and enabled homeowners to adopt renewable energy.

Early investors in the US residential solar sector, ourselves included, benefited from the tightening of spreads between 2022 and the end of 2024, as it moved into the mainstream. Higher interest rates have posed significant headwinds, though. Elevated rates have diminished the value proposition of renewable energy systems to consumers, despite rising electricity prices, resulting in lower origination volumes for solar ABS issuers. Higher rates have also increased financing costs.

To compensate for reduced loan origination volumes, certain solar ABS issuers loosened their underwriting standards. Issuers also continued to offer low-interest rate loans well into 2023 even as they faced significantly higher financing costs in the securitization markets.3 Two of the largest, SunPower and Sunnova Energy, have filed for bankruptcy over the past 12 months as they have been unable to fulfil their debt obligations. Others look set to follow.4

Looking ahead, the Trump administration’s efforts to accelerate the phase-out of clean energy tax credits under the ‘One Big Beautiful Bill’ Act will negatively impact future residential and commercial solar projects.5 This will likely result in a substantial decrease in solar loan originations, shrink the overall market and skew it towards third party originations in leases and power purchase agreements. We are seeing lower solar ABS issuance in 2025, with only $1.6bn issued by the end of May, compared with 2024’s record issuance of over $5bn.6

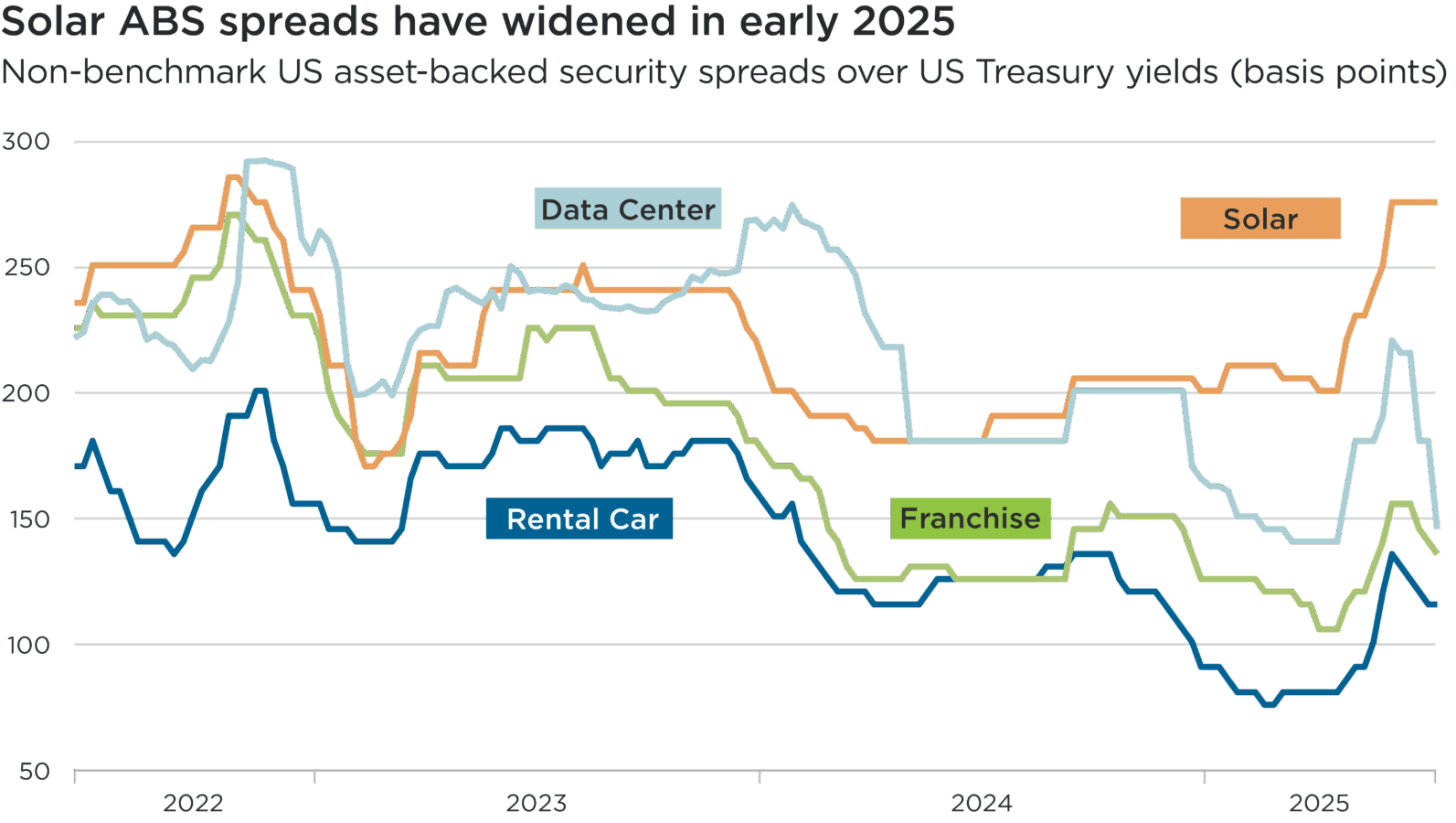

Source: BofA Securities, 30 May 2025. Spreads reference the Class A Notes of each sector, which have a five-year weighted average life and credit ratings that range from ‘AAA’ to ‘BBB’

Subhead: Non-benchmark US asset-backed security spreads over US Treasury yields (basis points)

Overview: This line chart shows the yield spreads of four non-benchmark US asset-backed securities (ABS) sectors, with similar ratings and weighted average lives, over the three years to the end of May 2025. It compares the spreads of solar ABS with data center, franchise and rental car ABS.

Overall, this chart illustrates the sharp increase in solar ABS yield spreads, relative to those of data center, franchise and rental car ABS, since late 2024. The yield spread between solar ABS and these comparable assets exceeded 100 basis points in May 2025, having broadly moved in tandem until late 2024.

Drivers of declining credit quality

Recent solar loan ABS issuances exhibit more credit risk in three ways.

First, they are facing higher and rapidly increasing delinquencies as a product of looser underwriting standards employed by certain issuers in 2022 and 2023, in particular. The underlying solar loan borrowers are also pressured by persistent inflation, with loans backing recent vintage ABS exhibiting the most stress.

Second, the structural credit protections in these recent securitisations are weaker, in part, because the transactions are structured to rely on fast prepayments from the underlying borrowers to build credit enhancement.7 Slowing prepayments have caused the total credit enhancement on the notes to decline, exposing investors to greater risk of losses.

Third, the financial viability of certain solar issuers has posed additional risks, heightening the risk of servicing disruptions, and higher operations and maintenance costs in the future, which can negatively impact ABS cashflows. Certain transactions’ anticipated repayment date (ARD) feature puts further financial pressure on solar issuers in a rising rate environment.8

These three factors have driven a sharp widening in solar ABS spreads in early 2025. As shown above, spreads have widened significantly compared to three other non-benchmark US ABS sectors, with similar ratings and weighted average lives, with which they have historically been well correlated.9

The impact of rising mortgage rates

Prepayments are an underappreciated credit risk in solar loan ABS.

Solar loan prepayments are correlated with turnover in the US housing market and residential mortgage rates. This is because the loans are secured by a ‘UCC-1’ filing on the house, requiring full repayment when a house is sold, or in some cases, when the mortgage loan is refinanced.10

As mortgage rates have increased, slower solar loan prepayments have led to declining credit protections on the subordinate tranches of certain solar ABS. Federal investment tax credits, which kick in on month 18 and incentivise borrowers to prepay up to 30% of the solar loan, were not always used for this purpose, causing these loans to re-amortise to a higher monthly payment amount. Lower prepayments, in combination with rising delinquencies from the collateral pool, have resulted in weaker credit protections, and in some cases, principal losses, on certain ABS notes. In turn, this has prompted rating agency downgrades.

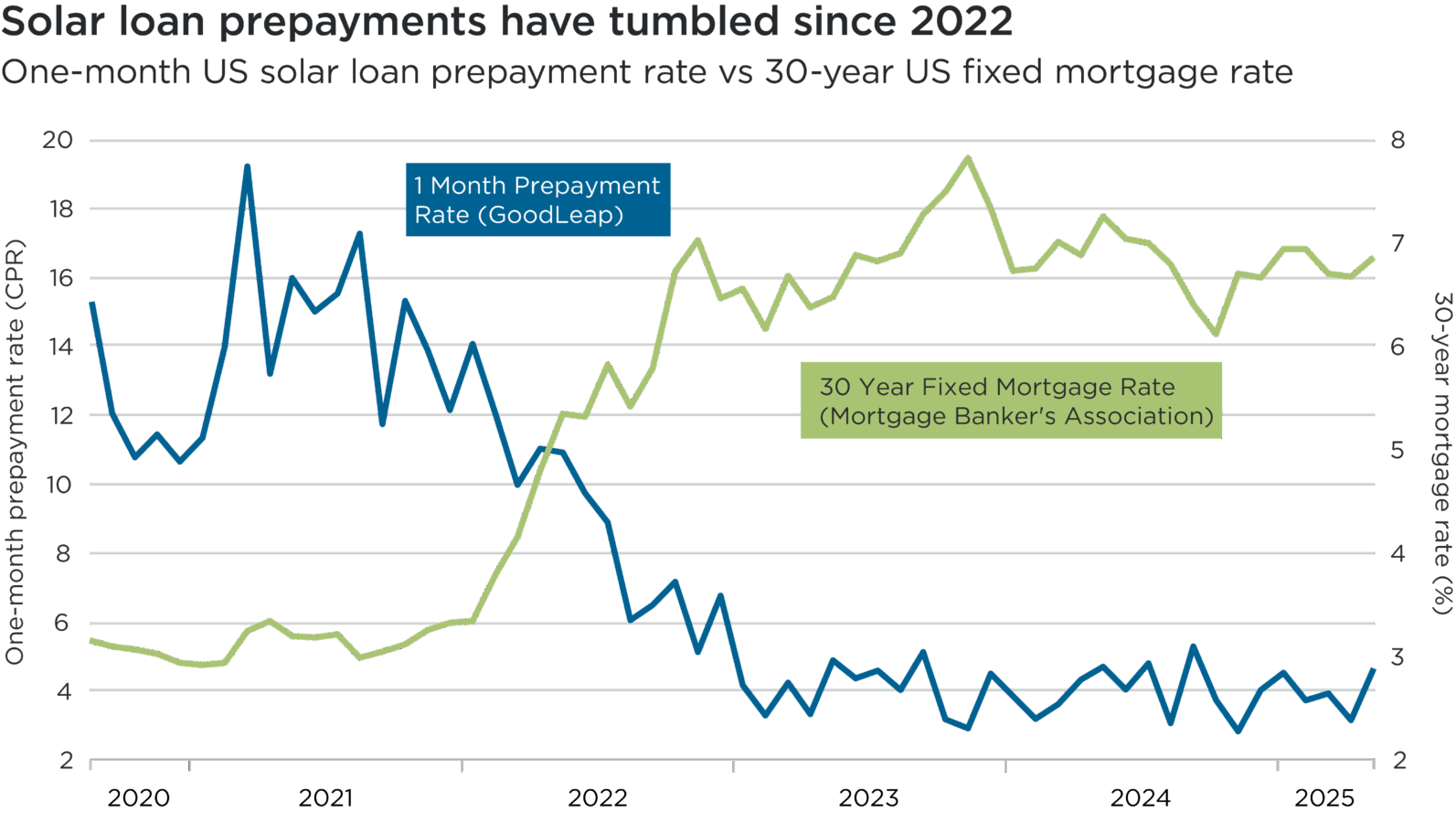

Source: Bloomberg, 30 May 2025.

Subhead: One-month US solar loan prepayment rate vs 30-year US fixed mortgage rate

Overview: This line chart compares the one-month US solar loan prepayment rate and the 30-year US fixed mortgage rate over the five years ending May 2025.

Overall, this chart illustrates the inverse relationship between these two metrics. As mortgage rates rose sharply in 2022, solar loan prepayment rates correspondingly fell sharply.

Identifying rays of opportunity through selectivity

The current downturn in the solar ABS market may put some credit investors off the asset class. It is our conviction that opportunities remain, though: elevated spreads mean solar ABS can offer attractive relative value compared to other securitized products.

We generally prefer earlier vintage solar ABS as the transactions are rated more conservatively and have stronger structural protections. Additionally, the borrowers of the underlying loans in these transactions benefit from low locked-in mortgage rates and high home price appreciation, which serve as buffers against loan losses. Older solar loan ABS are also unaffected by the proposed phase-out of clean energy tax credits, as the underlying borrowers have already monetized their tax credits. There do, however, remain risks related to sponsor strength and potential servicing disruptions in some cases.

Selectivity is therefore imperative in the current context. Investors who do not pay attention to the detail of individual issuances, especially more recent ones, risk flying too close to the sun.

1 BofA Securities, 30 May 2025

2 As at publication. The Trump administration’s ‘One Big Beautiful Bill Act’ has proposed phase outs to the 30% federal investment tax credit for residential solar installations by 31 December 2025 (Section 25D of the Inflation Reduction Act). The bill has additional provisions that restrict the availability of tax credits for solar systems installed under leasing arrangements (Section 48E of the Inflation Reduction Act).

3 Yield supplement over-collateralization (YSOC) was built into transaction structures to address this asset liability mismatch. YSOC refers to an amount calculated to compensate for receivables in a pool that have interest rates below a specified threshold. It helps ensure that the overall yield of the loan pool meets the required rate by providing additional collateral.

4 Solar Mosaic, a fintech platform for US residential solar and energy efficient home improvements, voluntarily filed for Chapter 11 bankruptcy on 6 June 2025

5 US House Committee on Ways & Means, May 2025: The One, Big, Beautiful Bill. Under Section 112006, the expiration of residential clean energy credit will be accelerated to 31 December 2025.

6 Finsight, 30 May 2025.

7 Credit enhancement is the improvement of the credit profile of a structured finance transaction, or the methods used to improve the credit profiles of such products or transactions. Credit enhancement consists of overcollateralization, subordination, excess spread and reserve accounts, and is a crucial part of securitization. By enhancing the credit profile of the notes of a securitization, the securities can be rated higher, attracting more investors and lowering the cost of borrowing for the originator.

8 The anticipated repayment date (ARD) in solar ABS is a structural feature that incentives the issuer to prepay the notes in full on that payment date. If the transaction is not paid in full, post-ARD interest will accrue at the related post-ARD additional interest rate, which is significantly higher than the related note rate.

9 These four ABS sectors – solar, rental car, franchise and data center – are non-benchmark (144a) securities that are not included within the Bloomberg Barclays Aggregate Index.

10 A Uniform Commercial Code (UCC)-1 filing is a legal document used to publicly record a security interest in personal property. It protects the lender of the solar panels, ensuring they can recover their investment if the homeowner fails to make payments. In case of default, the lender can repossess the solar panels as collateral.

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.