United States

United States

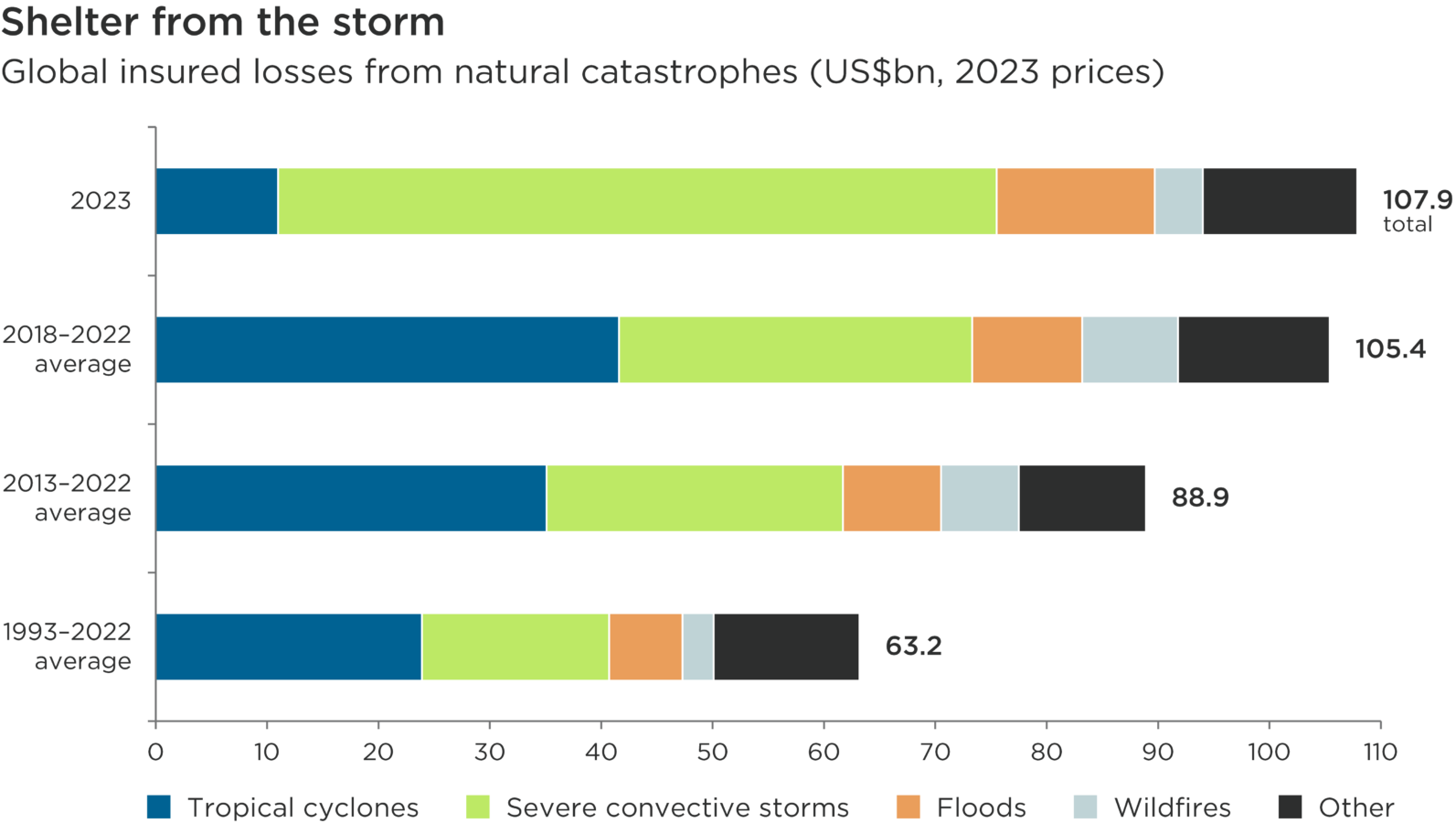

Category one: Tropical cyclones

Category two: Severe convective storms

Category three: Floods

Category four: Wildfires

Category five: Other

Overall, this chart illustrates the long-term upward trend in financial losses arising from natural catastrophes. It shows that tropical cyclones and severe storms have continued to account for the majority of losses over all time periods.

Shelter from the storm

Global insured losses from natural catastrophes (US$bn, 2023 prices)| Tropical cyclones | Severe convective storms | Floods | Wildfires | Other | Total | ||

|---|---|---|---|---|---|---|---|

| 2023 | 11.0 | 64.5 | 14.2 | 4.3 | 13.9 | 107.9 | |

| 2018–2022 average | 41.6 | 31.7 | 9.9 | 8.6 | 13.6 | 105.4 | |

| 2013–2022 average | 35.1 | 26.6 | 8.8 | 7.0 | 11.4 | 88.9 | |

| 1993–2022 average | 23.9 | 16.8 | 6.6 | 2.8 | 13.1 | 63.2 |

Source: Swiss Re Institute, January 2024. Figures rebased to 2023 prices.

The reinsurance industry is more financially exposed than most to the rising costs of climate change. Yet as the value of global assets at risk from extreme weather rises, the sector – in its role as a backstop for the insurance industry – is presented with an expanding opportunity set, especially if today’s protection gap can be reduced.

This may seem counterintuitive in the context of expanding payouts related to natural catastrophes. Despite being a relatively quiet year for hurricanes, global insured losses totalled US$108bn in 2023, above long-term averages in real terms. A record number of insured natural catastrophes last year – 142 – led to an additional US$172bn in uninsured losses, according to research by the Swiss Re Institute.1

Not all of these events were climate-related, but rising temperatures are accelerating the water cycle and contributing to more frequent and intense tropical cyclones and convective storms (or thunderstorms), and so flooding. They also increase the likelihood of heatwaves and droughts, magnifying wildfire risks.2 The human and financial costs of these events are amplified by demographic and economic trends: 29% of the increase in insured losses arising from severe US convective storms between 2008 and 2023 has been attributed to urbanisation.3

Pricing physical climate risks

Reinsurers face growing liabilities as exposure to natural catastrophe-related losses mounts. As a result, the industry has invested heavily in climate models to project when and where potential losses are most likely to occur. These insights can contribute to better-informed decisions in pricing physical climate risks.

After a period when several reinsurers mispriced these risks, eroding investment returns, the industry has tightened underwriting terms over the past two years. Reinsurers like German-listed Hannover Re and US-listed Renaissance Re have successfully increased deductibles, effectively passing more financial risk onto primary insurers. This is driving up premiums for policyholders as insurers pass higher costs on to businesses and households.4 In some higher-risk markets, like fire insurance in parts of the western US, many insurers no longer offer coverage.5

More accurate pricing of climate-related risks by reinsurers can ultimately contribute to climate adaptation efforts. For instance, more expensive (or unobtainable) home insurance should inform housebuilding trends away from areas vulnerable to rising sea levels, surface flooding or wildfires. Innovative insurance solutions, including incentivising policyholders to take measures like installing anti-flood doors or managing flammable vegetation, could meanwhile help improve climate resilience.

The industry’s capacity to influence behaviour and promote adaptation and resilience is often blunted by policies that distort insurance markets. Policymakers can, however, discourage new development in high-risk areas while extending cover to owners of assets that could become stranded. The UK’s Flood Re scheme, for instance, subsidises insurance in flood-prone areas for homes built before 2009 but not for new-builds (though 8% of UK homes built over the past decade have been in high-risk areas).6

Closing the protection gap

In less developed markets, many of which are among the most vulnerable to rising natural catastrophe-related risks, insurance coverage is typically much lower. Parametric insurance products, in which pre-defined payouts follow pre-determined conditions being met, can promote access to insurance and so help improve resilience.7

The global protection gap – the difference between insured and uninsured losses – highlights the size of the addressable market for the reinsurance industry. According to Swiss Re, 43% of economic losses from natural catastrophes in North America between 2014 and 2023 were uninsured. In Asia, this figure was 85%.8

As losses arising from natural catastrophes continue to rise, reinsurers are poised to play an increasingly important role in underwriting the physical climate risks facing households and businesses. So long as the industry prices these risks accurately, we believe it is well positioned to profitably contribute to the much-needed acceleration in climate adaptation and resilience over the decades ahead.

1 Swiss Re Institute, March 2024: New record of 142 natural catastrophes accumulates to USD 108 billion insured losses in 2023

2 Met Office, 2024: Effects of climate change

3 Swiss Re Institute, January 2024: Sigma 01/2024: Natural catastrophes in 2023

4 US Senate Committee on Banking, Housing and Urban Affairs, September 2023: Rising Insurance Costs and Reduced Coverage Hurt Homeowners, Renters

5 Lopez, N., et al., 10 May 2024: Beverly Hills 90210 Mansions Lose Fire Coverage as Insurers Flee. Bloomberg

6 Aviva, January 2024: One in thirteen new homes built in flood zone

7 Biffis, E., et al, 2022: Parametric insurance and technology adoption in developing countries. The Geneva Risk and Insurance Review

8 Swiss Re, March 2024: How big is the protection gap from natural catastrophes where you are?

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.