United States

United StatesThe successful deployment of vaccines within a year of the COVID-19 pandemic’s onset underscored the imperative of rapid, effective drug development.

As well as saving lives threatened by a virus that has killed an estimated 22 million people worldwide, mass vaccination enabled the safer reopening of societies from lengthy – and costly – lockdowns.1 The IMF estimates that the cumulative economic gain of a successful global vaccine rollout could add up to around US$9 trillion by 2025.2

Perhaps unsurprisingly, many have asked ‘why can’t all drug development be as swift and efficient as the COVID-19 vaccines?’ Pandemics aside, drug development remains a time and resource-intensive process. It can typically take a decade or more for a drug to complete three stages of clinical trials before being licensed. Most fail along the way.

To expedite the complex drug development process and leverage capabilities that they may not have themselves, pharmaceutical companies are increasingly turning to specialist partners.

As medical innovation continues to enable better treatments that improve health and quality of life for more people, we outline why we believe opportunities will be created for partners to the industry that find successful niches as the transition to a more inclusive, sustainable economy accelerates.

The rise of outsourcing

The pharmaceutical industry’s partners of choice for drug research, trials and commercial support are often contract research organizations (CROs).

Outsourcing certain activities to CROs is not a new phenomenon – Charles River Laboratories was established in Boston in 1947 to meet demand for lab rats. CRO capabilities, much like society’s attitudes towards animal testing, have advanced considerably over the past 75 years to meet the increasingly complex demands of the pharmaceutical industry and regulators.

According to analysis by McKinsey, the annual value of the global CRO market had risen to US$32bn in 2020, up from US$21bn in 2015.3 As scientific innovation continues to push boundaries, we believe two long-term drivers of this growth will continue.

First, innovations in medical science mean ever more specific conditions can be diagnosed, requiring increasingly niche knowledge and solutions. An increasingly complex drug discovery and development process broadens opportunities for CROs to add value, as they can maintain greater use of specialised infrastructure than any customer could alone.

Second, there are increasingly specialised and stringent requirements around the testing, manufacturing, and logistics of drugs. This creates opportunities for specialist partners to the pharmaceutical industry at different stages of the drug development process.

McKinsey expects the CRO industry to continue growing by an annual rate of 7.5% by 2025, driven largely by partnerships with emerging biotechnology companies that are increasingly at the cutting-edge of drug research.

The advent of advanced therapies

Recent advances in scientific innovation have led to the emergence of groundbreaking ‘advanced therapies’. These are medical products that use gene therapy, cell therapy or tissue engineering to treat diseases or injuries.

Cell therapy aims to treat diseases by restoring or altering certain sets of cells or by injecting cells to carry a treatment through the body. These cells, which may come from a donor or the patient, are cultivated or modified outside the body before being injected. Gene therapy, meanwhile, aims to treat diseases by replacing, deactivating or introducing genes into cells, altering the patient’s genetic code to recover the functions of critical cellular proteins.

Cell and gene therapies often target historically neglected ‘orphan’ diseases that are relatively uncommon but carry high unmet medical needs. Five years since the first cell therapy was approved for use in the US in 2017, more than 20 cell or gene therapy products have now been approved in the world’s largest drug market.4

Approved advanced therapies target illnesses including spinal muscular atrophy, retinal dystrophy and several rare forms of cancer. Among these are several CAR-T-cell therapies that have demonstrated the potential to eradicate very advanced leukemias and lymphomas. They work by reprogramming the patient’s own immune system cells which are then used to target their cancer.

Advanced therapies have the potential to deliver enormous health benefits to those afflicted by chronic illnesses. Where they can cure illnesses that currently require expensive and chronic treatment, they can also reduce long-term costs to health systems, insurers and wider society, despite often being very expensive. Cancer-targeting therapies Abecma and Kymriah, produced by pharmaceutical groups Bristol Myers-Squibb and Novartis respectively, carry list prices above US$400,000 per patient, per course.

Yet the high price tags carried by advanced therapies can be justified by the long-term cost-savings they can achieve. For example, research has found that Gilead’s cure for chronic hepatitis C – while priced at US$94,500 to US$150,000 per course – can deliver ongoing cost savings of up to US$1,500 per patient, per month.5

The advent of advanced therapies might also usher in a ‘payment revolution’, whereby drugmakers receive performance-related payment connected to patient outcomes. This represents an opportunity to better align the interests of drugmakers, insurers and patients, and to offer an antidote to resistance towards high-cost drugs that could hold back expensive scientific innovation.

Opportunities in bringing advanced therapies to market

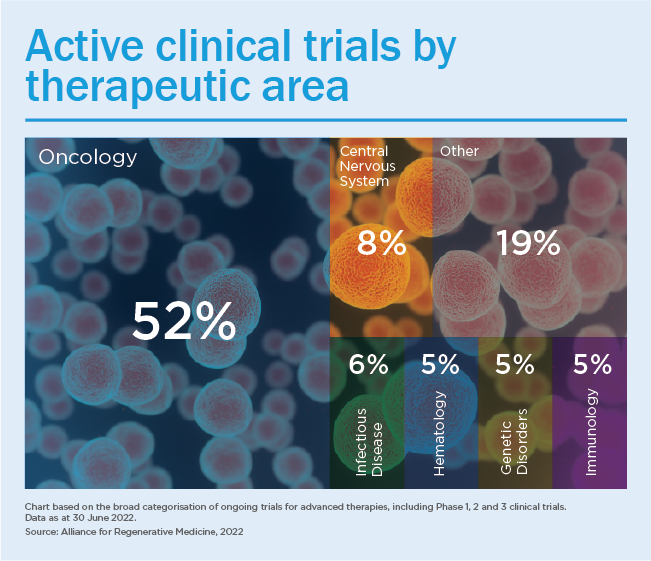

More than 2,000 trials for advanced therapies, around half of which target cancers, were ongoing globally at the end of June 2022.6 Only a minority will end up being approved, but this illustrates the scale of innovation underway. The global advanced therapy product market was estimated at US$7.9 billion in 2020 and is forecast to expand at an annual rate of 13.2%, almost tripling in value by 2028.7

As well as being a fast-growing market, the high-value and resource-intensive nature of advanced therapies creates higher-margin opportunities for outsourcing at four stages across the drug development process.

- Research – Especially low tolerances for medical impurities in cell and gene therapies makes collaborating with a specialist research partner necessary for some drug developers with limited in-house capabilities or experience. This is true of many smaller biotech companies that rely on CROs given their own relative lack of drug development infrastructure. Looking ahead, the use of ‘panomics’ – the integration of complex data to improve understanding of diseases – could significantly enhance both target identification and lead asset selection. Specialist partners to the industry will be well-placed to capitalise on this opportunity.

- Clinical trials – Drug trials that target rarer or more specific medical issues need to identify smaller niches of sometimes hard-to-find patients. CROs can leverage in-house data as a competitive moat in the running clinical trials: US-based IQVIA has access to more than 1.2 billion anonymised patient records worldwide, with analytics allowing it to select the most optimal and diverse patient cohorts on behalf of pharmaceutical groups. With such capabilities, it has run over 300 clinical studies related to rare and ultra-rare diseases since 2016.8 Decentralised clinical trials – which involve the use of remote assessments and at-home tests – can also ensure better representation of the global patient cohort, while simultaneously reducing costs and false negative results. This improves effective drug discovery and more equitable health outcomes.

- Patient monitoring – Higher regulatory requirements for advanced therapies often stipulate the need for enhanced monitoring of patient outcomes. We expect this to create opportunities for CROs that can apply their experience and technology to improve patient safety and deliver efficiencies for the industry – clinical monitoring can account for up to half of study costs. IQVIA applies predictive analytics to proactively identify patient risks.

- Drug transportation – Cell and gene therapies demand precise, temperature-controlled transportation that protects the integrity of high-value products. US company Cryoport is a leading ‘cold chain’ logistics partners for the life sciences industry, supporting more than 600 active cell and gene therapy clinical trials and the transportation of several approved products.9

Secular trends supporting specialist partners

We expect the long-term investment case for niche partners to the pharmaceutical industry to be supported by three major secular trends.

First, ageing global demographics should continue to lead to more investment in drug research and development (R&D) much as it is driving higher overall spending on healthcare. According to the OECD, healthcare spending is forecast to outpace GDP growth in almost all developed economic this decade, reaching 10.2% of GDP in OECD countries by 2030, up from 8.8% in 2018.10

Second, smaller and ‘virtual’ biotech companies are expected to continue playing a growing role in the development of advanced therapies. Biotech firms have a large share of advanced molecules in development across areas including cell and gene therapy, and McKinsey forecasts their R&D spending will grow by 8% a year to 2025 – twice the rate of the 15 largest global pharmaceutical groups.11

Third, financial incentives to bring treatments to market as soon as possible continue to put pressure on accelerating clinical development times. Even for larger pharmaceutical groups, who have historically had end-to-end development capabilities in-house, contracting out parts of the process can save time and money. In the case of a ‘blockbuster’ drug (that generates annual sales of US$1 billion or more), accelerating regulatory approvals by even a few months could eventually yields billions of dollars in extra sales before patent protections end. Recent changes in US legislation that will reduce patent lives for some drugs only contribute to this trend.

By enabling innovative treatments to be brought to market more quickly and efficiently, we believe specialist partners to the pharmaceutical industry can do more than find successful niches – they can also make a material contribution to addressing some of global society’s most severe healthcare issues.

Important information

The securities mentioned in this document should not be considered a recommendation to purchase or sell any particular security and there can be no assurance that any securities discussed herein are or will remain in strategies managed by Impax. Impax makes no representation that any of the securities discussed were or will be profitable, or that future investment decisions will be profitable.

As at 31 October 2022, Bristol-Myers Squibb was 1.9% of the Global Women’s Leadership strategy, 1.4% of the US Large Cap strategy and 2.0% of the US Sustainable Economy strategy; Charles River Laboratories was 0.1% of the US Sustainable Economy strategy; Cryoport was 0.5% of the Specialists strategy and 1.4% of the US Small Cap strategy; Gilead Sciences was 0.4% of the Global Women’s Leadership strategy; IQVIA was 3.9% of the Global Opportunities strategy and 2.3% of the US Large Cap strategy; and Novartis was 0.7% of the Global Women’s Leadership strategy. Portfolio holdings are subject to change.

1Economist, 21 September 2022: The pandemic’s true death toll

2International Monetary Fund, 2021: A Proposal to End the COVID-19 Pandemic

3McKinsey & Company, 2022: CROs and biotech companies: Fine-tuning the partnership

4US Food & Drug Administration, 2022

5Kaplan, D. E., 2018: Cost/Benefit of Hepatitis C Treatment: It Doesn’t End with SVR

6Alliance for Regenerative Medicine, 2022: Regenerative Medicine – The Pipeline Momentum Builds

7Grand View Research, 2020: Advanced Therapy Medicinal Products Market Size, Share & Trends Analysis Report By Therapy Type, By Region, And Segment Forecasts, 2021 – 2028

8IQVIA, 2022

9Cryoport, January 2022

10OECD, 2019: Health spending set to outpace GDP growth to 2030

11McKinsey, 2022: CROs and biotech companies: Fine-tuning the partnership