United States

United StatesA version of this article was first published in Pensions & Investments.

The research into diversity and its impact on financial performance has been widely reviewed and accepted. After years of building an extensive internal gender dataset, we decided to conduct our own research to see whether there might be more to that outperformance. We dug deeper, applying quantitative analysis to each of the factors in our proprietary gender score in order to answer one question – do companies that promote gender equity in leadership and workplace practices have better prospects for delivering alpha?

Our analysis found:

- Workplace equity factors – specifically pay equity and diverse talent pipeline initiatives – emerged as the most significant gender-related factors correlating with company performance

- One leadership factor – women in management – has been one of the biggest indicators of company outperformance or contributors to alpha

The conviction behind our analysis

We know that companies with diverse decision making have historically performed better than those with homogenous boards and executive teams. Study after study has shown this and we highlight the latest research each year in our Business Case for Diversity paper. We have the highest conviction in that business case. This is why we have invested for more than 15 years in companies that lead on gender diversity.

In 2014, our Gender Analytics team created a proprietary tool, the Impax Gender Score, by building out a custom dataset using a combination of publicly available and third-party diversity data. We have been adding to that dataset ever since, as more company information becomes available with respect to both gender-diverse leadership and other measures of gender equity. While newer datasets do not stretch back to 2014, they still provide useful insights into the contribution that gender equity can make to financial performance.

The criteria below are the primary components of the Impax Gender Score, which we use to rank each company in the MSCI World Index.1

Factors in Impax Gender Score2

| Leadership Factors | Workplace Equity Factors |

|---|---|

| Women in Executive Management | Demographic Data Disclosure |

| Women on the Board | Diversity Targets |

| Female CEO | Diverse Talent Pipeline Initiatives |

| Female CFO | Pay Equity Initiatives |

| Female Board Chair | Signatory to UN Women's Empowerment Principals |

Analysis of our growing data set has yielded fresh insights into the impact of individual factors. With other potential drivers stripped away, we were able to determine which factors provided the strongest alpha signals over time.

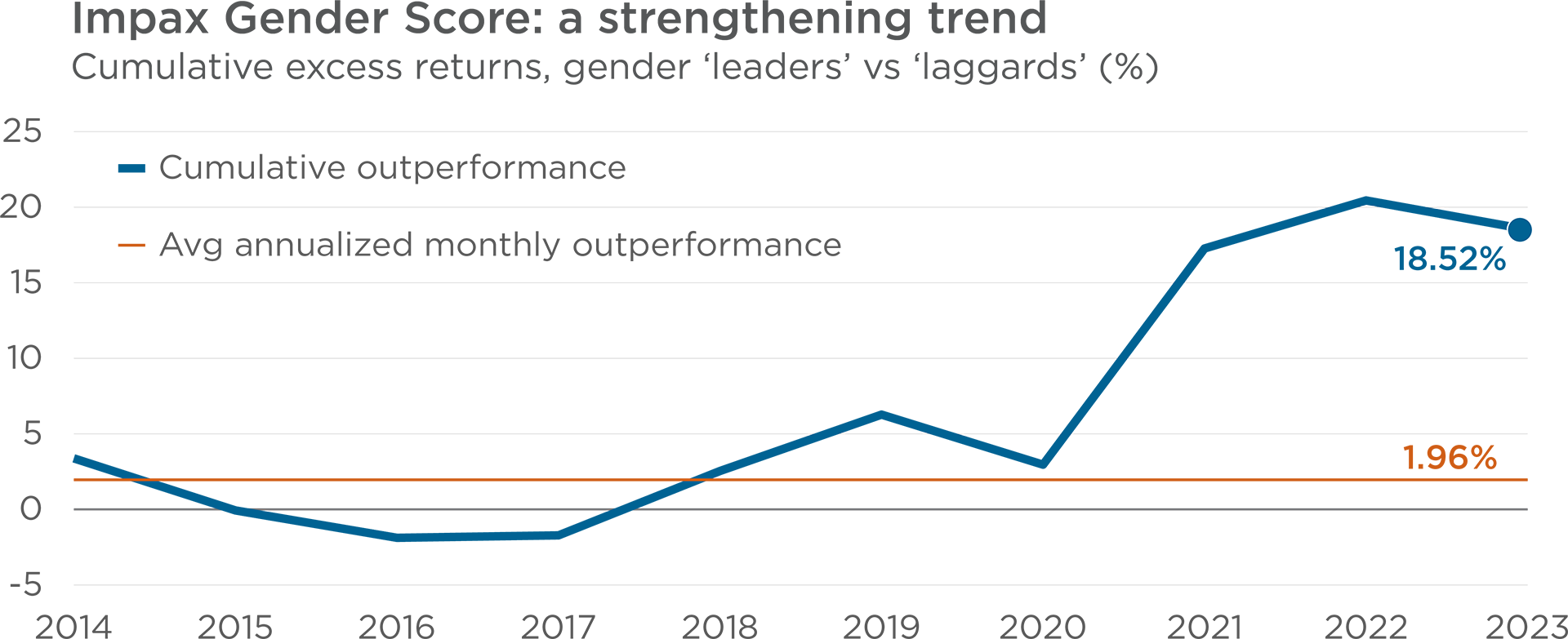

Gender leaders outperform gender laggards

First, we looked at the Impax Gender Score rankings and measured the performance of the ‘leaders’ (MSCI World companies with equal-weighted scores in the top 25%) versus the ‘laggards’ (bottom 25%). The chart below shows the difference in cumulative excess returns between the two groups from June 2014 to February 2023.

This graph is intended to show the effectiveness of the lmpax Gender Lens when used as a screening tool to evaluate the performance potential of securities within the MSCI World Index based on their lmpax gender scores. There is no guarantee that these trends will continue, and these scores are a single consideration in the investment process. This graph does not represent performance of any product or managed account strategy. No representation is being made that any account will or is likely to achieve results similar to those shown. Past performance is not a reliable indicator of future performance. Past performance does not predict future returns. Source: FactSet as of 2/28/2023. The data shown here is the equal weighted, cumulative monthly excess return of the top quartile of MSCI World Index companies verses the bottom quartile based on their lmpax Gender Score for the period of 6/30/2014 – 2/28/2023. Data shown is one month forward returns. Indexes are unmanaged and not available for direct investment.

Gender leaders have delivered significantly higher returns than gender laggards, particularly since 2020. Annualized monthly returns for these companies were, on average, two percentage points higher for the period.

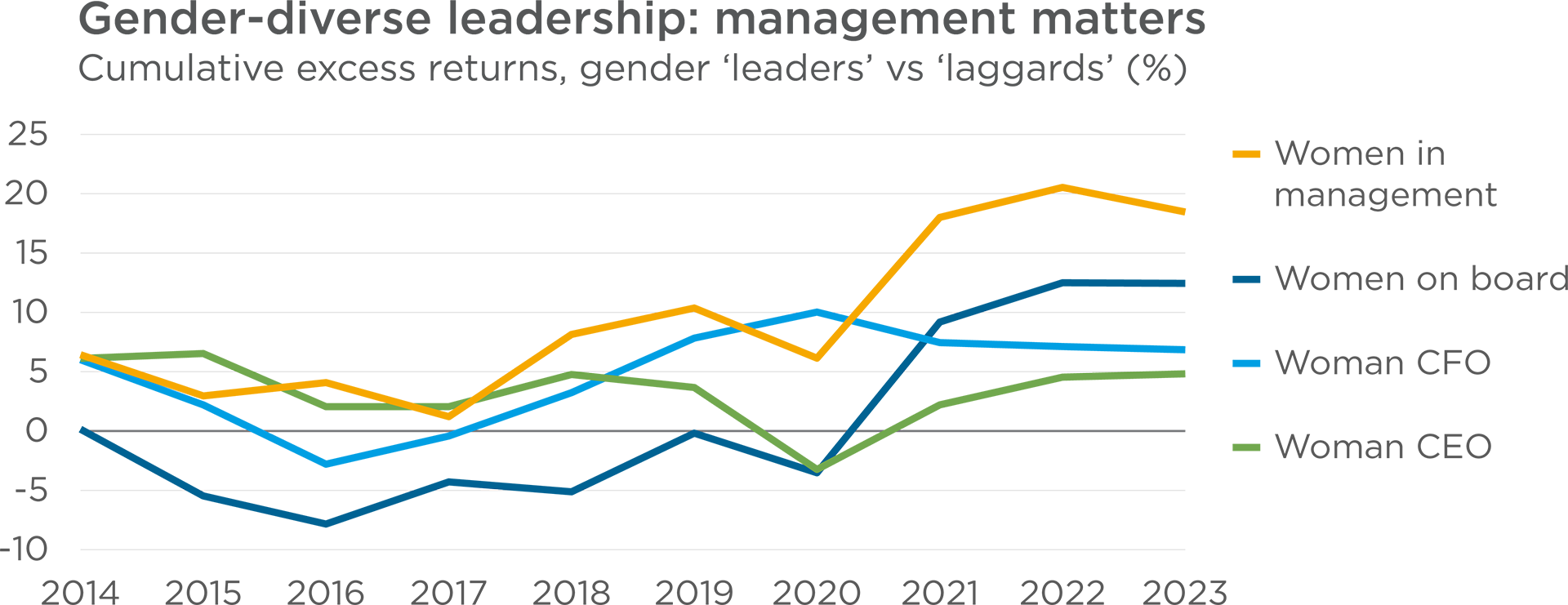

Diverse leadership counts – especially in management

Second, we disaggregated the data to gain a deeper understanding of how each gender factor has contributed to financial performance. The chart below reveals the impact of the four leadership factors with the biggest difference between leaders and laggards : women in management, women on the board, woman chief financial officer (CFO) and woman chief executive officer (CEO).3

Gender leadership factors represent the top quartile of companies vs the bottom quartile of companies. This graph is intended to show the effectiveness of the lmpax Gender Lens when used as a screening tool to evaluate the performance potential of securities within the MSCI World Index based on their lmpax gender scores. There is no guarantee that these trends will continue and these scores are a single consideration in the investment process. This graph does not represent performance of any product or managed account strategy. No representation is being made that any account will or is likely to achieve results similar to those shown. Past performance is not a reliable indicator of future performance. Past performance does not predict future returns. Source: FactSet as of 2/28/2023. The data shown here is the equal weighted, cumulative monthly excess return of the top quartile of MSCI World Index companies who do or don’t (yes or no) meet the following gender leadership criteria – women on board, women in management, woman CFO and woman CEO versus the bottom quartile based on their lmpax Gender Score for the period of 6/30/2014 – 2/28/2023. Data shown is one month forward returns. Indexes are unmanaged and not available for direct investment.

The impact of each of these four leadership factors has trended upward since 2016, but the strongest relationship with shareholder returns is clearly women in management. This aligns with the academic and financial literature: diverse executive leadership is likely to be positively correlated with financial performance.4 While leaders and laggards on board gender diversity did not deliver returns that were as divergent, our analysis did reveal that being in the bottom quartile for this factor is predictive of worse financial results.5

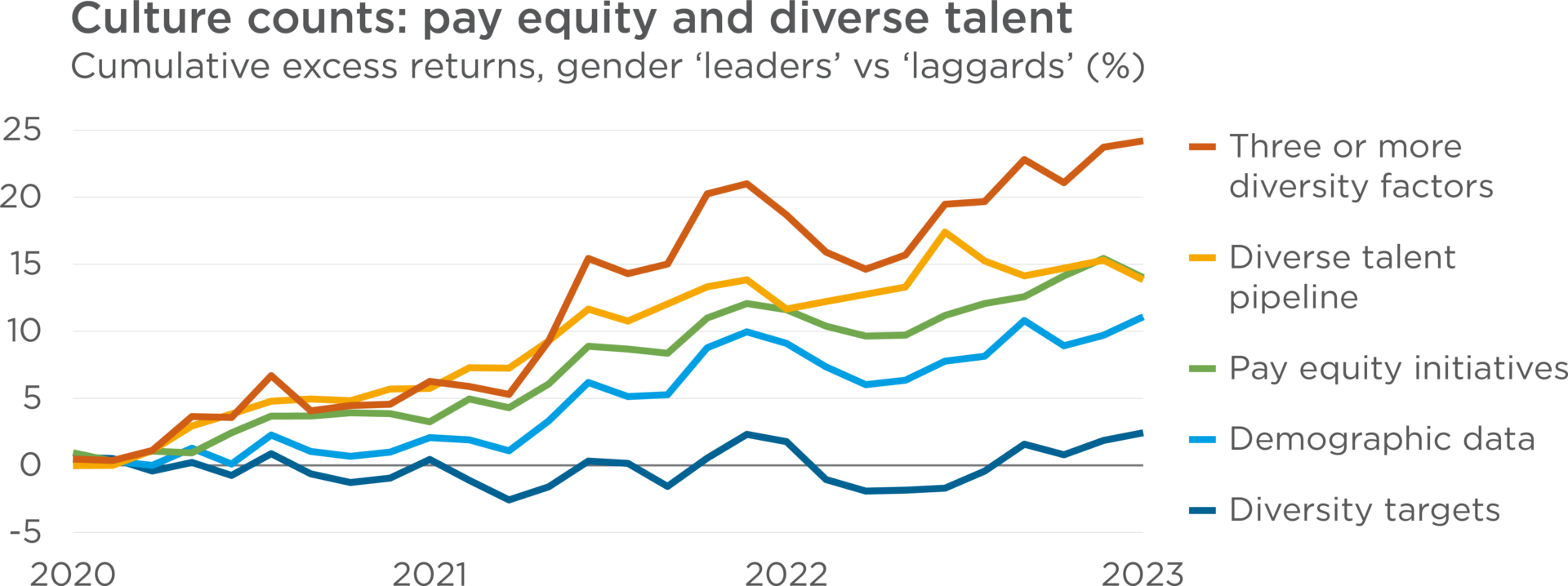

Workplace equity factors emerge as source of alpha

Third, we analyzed excess shareholder returns associated with several key workplace equity factors. The chart below summarizes the outperformance associated with four of these factors, for which data is available going back to 2020.

Workplace equity factors represent the top quartile of companies vs the bottom quartile of companies. This graph is intended to show the effectiveness of the lmpax Gender Lens when used as a screening tool to evaluate the performance potential of securities within the MSCI World Index based on their lmpax gender scores. There is no guarantee that these trends will continue and these scores are a single consideration in the investment process. This graph does not represent performance of any product or managed account strategy. No representation is being made that any account will or is likely to achieve results similar to those shown. Past performance is not a reliable indicator of future performance. Past performance does not predict future returns. Source: FactSet as of 2/28/2023. The data shown here is the equal weighted, cumulative monthly excess return of the top quartile of MSCI World Index companies who do or don’t (yes or no) employ the following policies or practices – pay equity initiatives, diversity targets, diverse talent pipeline and demographic data versus the bottom quartile based on their lmpax Gender Score for the period of 11/30/2020 – 2/28/2023. Data shown is one month forward returns. Indexes are unmanaged and not available for direct investment.

Most of the workplace equity factors are positive for this three-year period, particularly talent pipeline and pay equity initiatives. Companies with three or more of these indicators tend to outperform those with two or fewer. While this is unsurprising to us, it underscores how specific practices provide a window into culture, and strong cultures tend to contribute to better performance.

Drawing lessons from our research

We believe investing in gender leaders and avoiding gender laggards has consistently added value over time. Our research reinforces that inclusive cultures and purpose-driven business practices can be contributors to outperformance. Companies that incorporate these practices tend to attract and retain talented employees from diverse backgrounds who can then drive innovation, productivity, customer loyalty and resilience. In our view, such improving corporate cultures will be a crucial element in the transition to a more sustainable economy.

The Impax Gender Analytics Team’s expertise and quantitative insights will help us continue navigating these evolving gender-related indicators and long-term societal trends. Companies that value diversity and promote equitable workplace practices stand to benefit. We will continue to focus on identifying and investing in those companies.

1 The MSCI World Index captures large and mid-cap representation across 23 developed markets. With 1,509 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

2 This a partial list of the factors included in our proprietary data set.

3 ‘Women in management’ is defined by the Impax Gender Analytics team, who identify the top decision makers at each company where we track this data.

4 Impax, 2022: The Business Case for Diversity

5 The bottom quartile for ‘women on the board’ consists of companies whose boards have less than 23% women. This group’s average 12-month underperformance relative to the MSCI World Index (ex-Energy) is -2.5%.

Important information

This material is solely for the use of institutional and professional investors. This material is being provided for informational purposes only. The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries, the material is provided upon specific request. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from Impax. The material does not constitute a distribution, an offer, an invitation, recommendation or solicitation to sell or buy any securities in any jurisdiction.

Impax Asset Management Group plc includes Impax Asset Management Ltd, Impax Asset Management (AIFM) Ltd., Impax Asset Management Ireland Ltd, Impax Asset Management LLC, and Impax Asset Management (Hong Kong) Limited (together, “Impax”).

Impax Asset Management Ltd, Impax Asset Management (AIFM) Ltd and Impax Asset Management LLC are registered as investment advisers with the U.S. Securities and Exchange Commission (“SEC”), pursuant the Investment Advisers Act of 1940 (“Advisers Act”). Registration with the SEC does not imply a certain level of skill or training.

The statements and opinions expressed are those of the author, as of the date provided, and may not reflect current views. While the author has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. This material may not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment decision.

This material contains past performance information. Past performance does not guarantee future results.

Impax is a trademark of Impax Asset Management Group Plc. Impax is a registered trademark in the EU, US, Hong Kong and Australia. ©Impax Asset Management LLC, Impax Asset Management Limited and/or Impax Asset Management (Ireland) Limited. All rights reserved.

Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.