United States

United StatesElectricity demand is soaring in Asia’s fast-growing economies, placing the region at the vanguard of the global electrification trend. Key to enabling this is the expansion of a reliable grid through advanced grid hardware and software, and power management and cooling solutions, creating opportunities for Asian technological leaders.

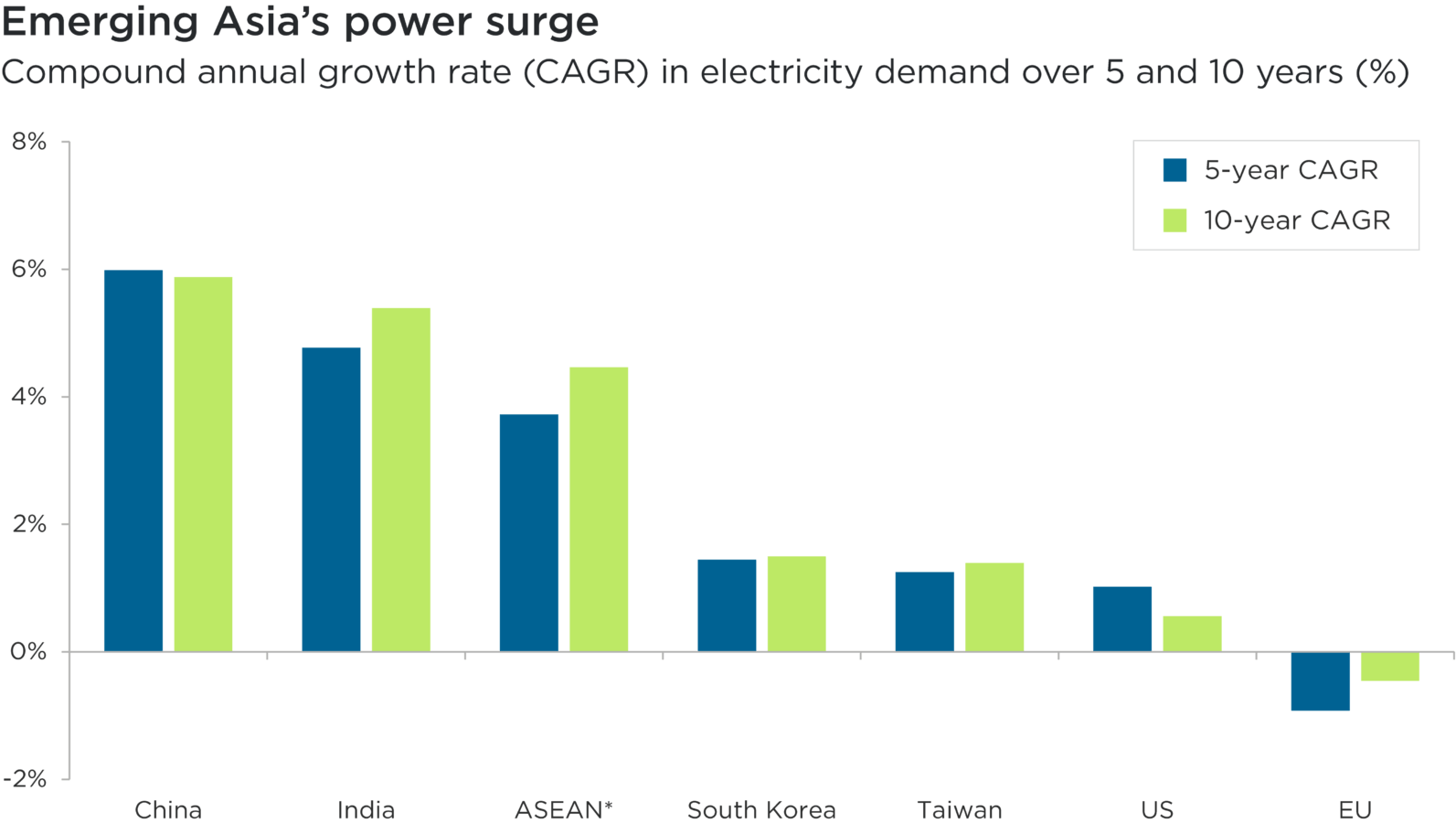

Subhead: Compound annual electricity demand growth over 5 and 10-year periods (%)

Overview: This bar chart compares the percentage increases in annual electricity demand, for five and ten year periods ending 2023, for major Asian economies, the US and the EU.

Category one: China

Category two: India

Category three: ASEAN

Category four: South Korea

Category five: Taiwan

Category six: US

Category seven: EU

Overall, this chart shows that electricity demand growth rates are significantly higher in China, India and the ASEAN economies of southeast Asia than in higher income Asian, US and European economies. Electricity demand has grown most rapidly in China, followed closely by India and ASEAN economies.

Source: Ember / Macquarie Research, April 2024. * The Association of Southeast Asian Nations (ASEAN) comprises 10 countries including Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam

Rising electricity demand

Asia is expected to consume 51% of the world’s electricity in 2025, up from 26% in 2000.1 This rise has been driven by China, which now accounts for 33% of global demand (10% in 2000) and consumes more electricity per person than the EU.2 Demand is now growing at comparable rates in India and the emerging ASEAN economies of southeast Asia.3

Expanding industrial activity, improving living standards and technological trends are all pushing up regional electricity consumption. Three of the largest individual drivers are space cooling, transport and data.

First, rising incomes and temperatures are fuelling a dramatic increase in sales of air conditioning (AC) units. On current trends, the IEA estimates that the number of AC units in southeast Asia alone could rise from 40mn in 2017 to 300mn by 2040, when space cooling could account for 30% of peak electricity demand.4

Second is the rapid adoption of electric vehicles (EVs), especially in China, by far the world’s largest EV market. Already consuming 0.7% of Chinese electricity demand, EVs could account for 6.8% by 2035 based on current policies.5

Third, the rise of artificial intelligence (AI) and data centre demand are structurally changing power market dynamics. China’s State Grid Energy Research Institute expects demand from the country’s data centres to double by 2030, versus 2020, and account for 3.7% of total electricity use.6

Grid and storage solutions

An accelerated expansion of Asia’s power grid infrastructure is needed to accommodate forecast demand growth and ensure resilience of supply over the coming decades. Rystad Energy has projected that roughly US$1.5tn of investment is needed between 2024 and 2030 in the region’s grids.7

Accelerated capital expenditure is directed towards both grid hardware and software. The region’s grids not only have to get bigger, but also smarter to accommodate the rise of more decentralised, intermittent renewable generation and bi-directional electricity flows with ‘prosumers’ who both consume and produce electricity, typically rooftop solar.

This ramp-up in spending supports demand for leading manufacturers of critical hardware, including transformers and high voltage grid equipment, such as Hitachi. The Japan-listed conglomerate is also a leading supplier of grid management software which is needed to more accurately track flows of power and changes in supply and demand, and to anticipate system vulnerabilities and equipment failures.

As intermittent renewables play a growing role in power generation, energy storage is increasingly important to match supply and demand and helps ensure grid stability. Storage systems enable smart load management and increase power quality for electricity transmission and distribution, by providing essential services such as frequency regulation, voltage support, and peak shaving.

Power management and cooling solutions

The high voltage loads required by data centres, which require consistent power supplies and efficient cooling systems to maintain operational efficiency, place significant demands on local grids. Higher temperatures exacerbate this challenge in Asia, where power usage efficiency tends to be higher than in other regions.8

Innovative power management solutions can ensure reliable supplies and reduce electricity consumption in this context. Investments to support the expansion of the region’s digital infrastructure support demand for products manufactured by the likes of Delta Electronics. The Taiwan-listed company is one of the largest suppliers of solutions to data centres and other sectors to ensure stable and energy-efficient power supplies.9

Delta is also a supplier of cooling systems to the industry. Given cooling accounts for approximately 40% of data centre power consumption, there is a large and growing market for companies whose products improve cooling efficiency.10 Liquid cooling systems, which are being developed by the likes of Delta and China-listed Shenzhen Envicool, are supplanting air-cooling systems in data centres. The global market for liquid cooling, which can reduce power needs and support higher server densities, is projected to expand from US$0.3bn in 2024 to US$7.8bn by 2027.11

Opportunities for enabling technologies

It is our conviction that the electrification of Asian economies presents significant opportunities for companies whose products and services improve grid resilience and enhance the operational efficiency of data centres. The pace of electricity demand growth in the region underscores how critical investments in these solutions will be for grid operators and major electricity consumers over the years ahead.

1 IEA, 2023: Electricity Market Report 2023

2 IEA, 2024: Electricity Market Report 2024

3 Ember / Macquarie Research, 2024. The Association of Southeast Asian Nations (ASEAN) comprises 10 countries including Indonesia, Malaysia, the Philippines, Singapore, Thailand and Vietnam

4 IEA, 2019: The future of cooling in southeast Asia

5 IEA, 2024: Global EV Outlook 2024

6 State Grid Energy Research Institute, 2021

7 Rystad Energy, 2024: Enable or inhibit: Power grids, key to the energy transition, require $3.1 trillion in investments by 2030

8 Jiao, Y. et al., 2017: Thermal Analysis for Underground Data Centres in the Tropics. Energy Procedia.

9 Delta Electronics

10 McKinsey, 2023: Investing in the rising data center economy

11 Macquarie Equity Research, April 2024

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.