United States

United StatesThe drive to decarbonise the world’s electricity system has so far focused on expanding ‘upstream’ energy supply, like solar and wind power generation. A record US$659bn was estimated to have been invested in new renewable energy capacity in 2023.1

Investment in the grid infrastructure needed to connect and manage more intermittent electricity supply has not kept pace. Meanwhile, electricity demand is growing and the risks of potentially devastating blackouts are rising.2

The expansion and modernisation of grids around the world will be essential to the transition to a more sustainable economy. More than US$21tn must be invested in the world’s grids by 2050 to support a global net-zero trajectory.3 Once deemed a ‘boring’ sector, we see a highly dynamic investment landscape now emerging.

A multi-trillion-dollar investment trend

Although investment in renewable energy generation has rapidly increased, capital flowing into the grids that transmit power over long distances and distribute it across local networks has been static, at around US$300bn a year.4

A combination of increasing electrification of end demand and higher economic growth in developing economies means that global electricity demand is set to triple between now and 2050.5 Annual global investment in electricity grids will need to rise commensurately, with annual spending of some US$900bn between now and 2050, plus an additional US$200bn directed towards expanding energy storage capacity.

Driving much of this anticipated growth is the electrification of processes that currently burn fossil fuels. For example, adoption of electric vehicles (EVs) is forecast to increase US electricity demand by as much as 13% this decade.6 Meanwhile, in the UK, a complete switch from natural gas boilers to electric heat pumps for domestic heating would double electricity demand during winter months.7

Electrifying industrial processes such as steel production and producing ‘green’ hydrogen for immediate use in refining and fertiliser production will also pressure electricity demand, as will the growth of artificial intelligence and the energy-hungry data centres that power it. In emerging markets, massive increases in access to reliable electricity are still needed to meet basic needs like space heating and cooling.

But demand growth is only half of the story. The power system of the future must become more intelligent for three reasons: decentralised capacity, intermittent generation and bidirectional electricity flows.

- First, low-carbon energy systems will be supplied by millions of generators, ranging in size from enormous wind and solar farms to individual rooftop installations. This is a stark contrast to the small number of large power plants that have dominated production to date.

- Second, more interconnections between grids and large-scale storage will be needed to manage the intermittency of solar and wind generation. Batteries will be both a source of electricity demand during periods of excess renewable generation and a source of supply for grid operators when it is dark and still.

- Third, electricity networks are also becoming bidirectional. More users are becoming so-called ‘prosumers’ who both consume and produce electricity. More flexible systems are needed to harness the vast potential for EVs to help balance the system by charging when electricity is abundant and cheap and discharging electricity when it is expensive.

Investment opportunities as grids modernise

Electricity networks need to get bigger and smarter, and be built faster. We see this global build-out creating investment opportunities across four broad sectors.

First are the developers and operators of grid infrastructure who typically command dominant positions in highly regulated markets. Second, the suppliers of critical materials and components who stand to benefit from structural demand growth in those materials. Third, providers of advanced IT systems who will be essential to the management of more complex grids. Finally, there are the energy storage companies that provide not just the technology itself, but also the innovative business models that increasingly need to balance electricity supply and demand.

1. Developers and operators

In markets like the UK and Spain, the integrated utilities which own and operate power grids can offer investors the prospect of consistent, regulated and inflation-linked returns. Grid operator revenues should rise in line with long-term growth in electricity usage, as a percentage of end user fees is typically given to transmission and distribution providers.

To prepare for this growth, these companies are increasing capital investments in grid infrastructure as they build capacity for rising electricity consumption and manage the addition of more geographically diverse and intermittent renewable generation to the system.

For example, UK-listed utility SSE announced in November 2023 that it is increasing its five-year capital investment programme to £20.5bn, focusing on electricity infrastructure to support its transition to net zero.8 Similarly, Spain’s Iberdrola recently announced plans to invest around €10bn in its UK power networks. By expanding their regulated asset base, grid operators lock in an increase in their revenue base.

Much of the additional capital expenditure by grid operators will flow to companies involved in engineering, procurement and the construction of electricity grids. By extension, companies like those that specialise in industrial equipment rental, such as Ashtead and United Rentals, stand to benefit from a structural uptick in demand for their services.

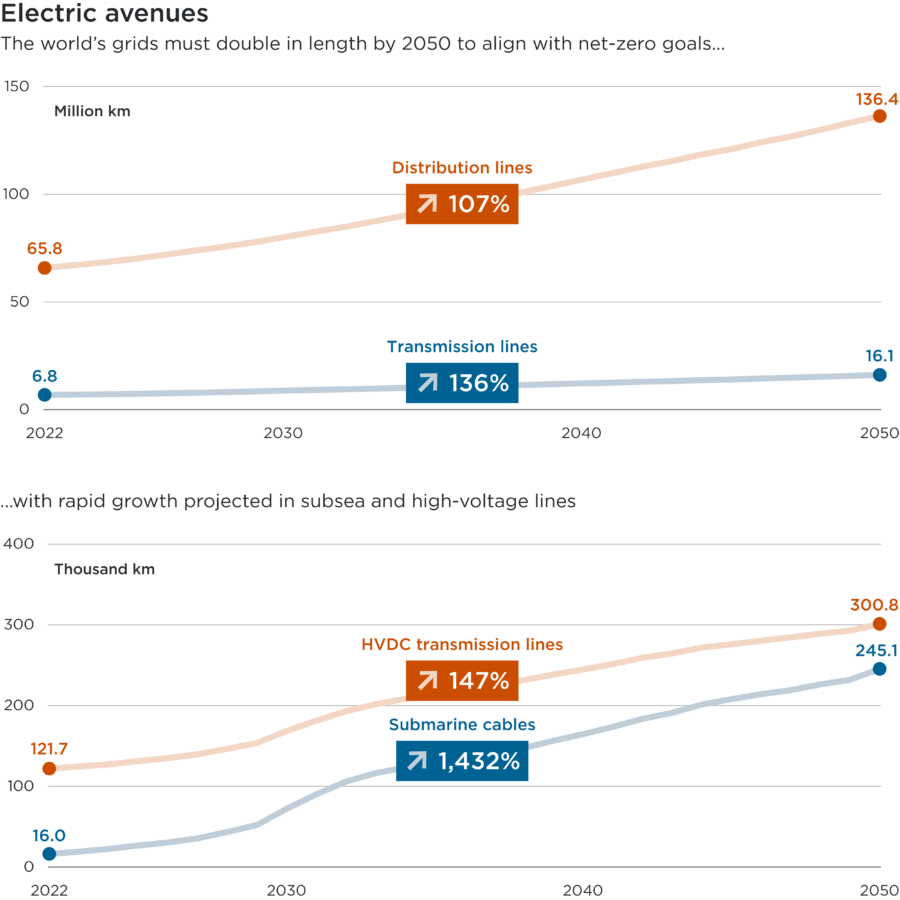

Source: BloombergNEF, March 2023. These projections are based on the Net Zero Scenario in BNEF’s New Energy Outlook, which maps a pathway to achieving net-zero emissions by 2050. ‘HVDC’ = High-Voltage Direct Current.

| Type | Unit | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 | 2036 | 2037 | 2038 | 2039 | 2040 | 2041 | 2042 | 2043 | 2044 | 2045 | 2046 | 2047 | 2048 | 2049 | 2050 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Transmission | million km | 7 | 7 | 7 | 7 | 8 | 8 | 8 | 8 | 9 | 9 | 9 | 10 | 10 | 10 | 11 | 11 | 11 | 12 | 12 | 13 | 13 | 13 | 14 | 14 | 14 | 15 | 15 | 16 | 16 |

| Distribution | million km | 66 | 67 | 68 | 70 | 72 | 74 | 76 | 78 | 80 | 82 | 85 | 87 | 90 | 93 | 96 | 98 | 101 | 104 | 107 | 110 | 113 | 115 | 118 | 121 | 124 | 127 | 130 | 133 | 136 |

| Submarine | thousand km | 16 | 19 | 22 | 27 | 30 | 36 | 43 | 52 | 72 | 90 | 106 | 116 | 123 | 129 | 135 | 140 | 147 | 156 | 165 | 173 | 184 | 191 | 201 | 208 | 214 | 219 | 226 | 232 | 245 |

| HVDC | thousand km | 122 | 124 | 127 | 131 | 135 | 140 | 146 | 154 | 168 | 181 | 193 | 202 | 208 | 215 | 220 | 226 | 231 | 238 | 245 | 251 | 259 | 264 | 272 | 276 | 280 | 284 | 289 | 293 | 301 |

Source: BloombergNEF, March 2023. These projections are based on the Net Zero Scenario in BNEF’s New Energy Outlook, which maps a pathway to achieving net-zero emissions by 2050. ‘HVDC’ = High-Voltage Direct Current.

Overview: This pair of line charts illustrates the projected growth in the length of electricity grid globally. The top chart illustrates the projected expansion of distribution and transmission lines to 2050. The bottom chart illustrates the projected rapid expansion of submarine and high-voltage direct current transmission lines to 2050.

Category one: Transmission

Category two: Distribution

Category three: Submarine

Category four: HVDC transmission lines

Overall, these charts show that all the length of all types of line are projected to rise rapidly by 2050.

Presentation

This pair of line charts illustrates the projected expansion in the length of electricity grid globally.

2. Materials

The world’s electricity network must double in length by 2050. BloombergNEF estimates that the network of overhead, underground and submarine cables will have to reach 152mn km to realise net-zero goals.9

On top of this, ageing grid infrastructure must be replaced: two-fifths of Europe’s grids are more than 40 years old.10 In the US, the average age of a large power transformer is similar, at the end of its typical lifespan.11

Regional networks of high voltage direct current (HVDC) cables will emerge to connect areas rich in renewable generation capacity with centres of demand. Advisory firm Xodus estimates that the offshore wind industry alone will create demand for 56,000km of HVDC cable by 2035, up from just 1,950km in 2020.12

This is a specialist market, where track record matters, especially for sub-sea cables. Market leaders like Prsymian can command strong pricing power. The Italian company is the world’s leading power and optical cable maker by revenue and the largest supplier of cables for the high-voltage transmission market.13 Prysmian, a vertically integrated fibre cable producer, also stands to benefit as more interconnector projects also require integrated data cables.

Laying cable over long distances is resource intensive. Early movers are using recycled materials and components to reduce the price volatility of commodity inputs like copper and reduce waste.

Meanwhile, higher power demand and the changing needs of a bidirectional grid will require extensive updates of distribution networks (used for moving electricity over shorter distances and at lower voltages than the transmission network). By 2035, US utilities may need to invest as much as US$1tn in distribution networks, on top of US$300bn to US$500bn in transmission lines.14 This ramp-up in spending will support demand for manufacturers of key components, including converters, transformers and voltage control equipment, such as Hubbell. The US company is a leading supplier of critical electrical hardware and services to North American utilities as they modernise their grids for the new economy.

3. System intelligence

As electricity grids become more complex, with increasingly distributed generation and the emergence of more ‘prosumers’, there is growing need for advanced systems to help manage them.

Modern smart grids make extensive use of sensors and the ‘internet of things’ to more accurately track flows of power and changes in supply and demand, and to anticipate system vulnerabilities and equipment failures. Artificial intelligence (AI) and machine learning help produce more accurate forecasts of supply and demand, support more flexible demand-side management technologies and increase the cybersecurity of vital electrical infrastructure.

Increased system intelligence relies on smart metering. Progress on installing smart meters ranges from 86% in Japan to 69% in the US and just 52% in the EU, as of 2021.15 The figures for the Middle East, Africa, South and Central America and India are meanwhile in single digits. Growth opportunities are clearly substantial. Even in mature markets, significant investment in smart grids is planned, with the EU planning to invest €170bn in grid digitalisation by 2030, for example.16

This is a supportive environment for suppliers of smart grid solutions such as Schneider Electric. The French group provides end-to-end software that enables more reliable and efficient grid management. For example, its demand management and grid metering solutions help utilities design and operate grids, using data to gain system insights and address variability.

4. Energy storage

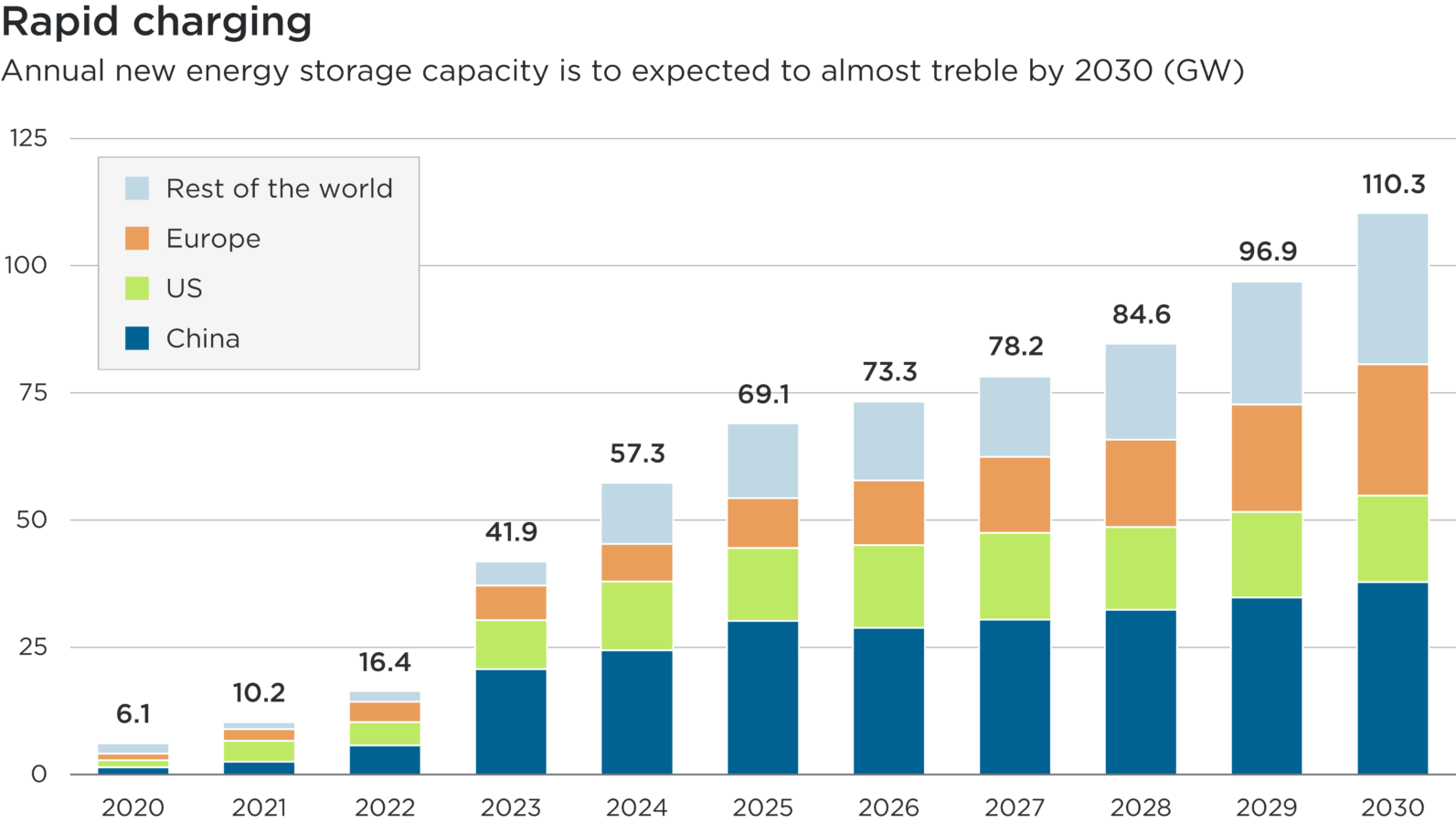

A key challenge posed by the transition to low-carbon grids is the intermittency of solar and wind generation. This is driving investment into a range of energy storage technologies, including utility-scale lithium-ion batteries, innovative solid-state batteries, longer-duration flow batteries, and well-established technologies such as pumped hydroelectricity. Bloomberg NEF forecasts that global energy storage capacity will grow at an annual rate of 27% between 2023 and 2030.17

Increasingly, new wind and solar farms are being developed with co-located battery storage, often to meet regulatory requirements. Utility-scale battery storage can contribute to a low-carbon grid through load-levelling (storing excess renewable generation), frequency regulation (balancing electricity supply and demand) and black start services (helping the grid recover from a full or partial shutdowns). Providing these valuable network services earns revenues for battery operators. Renewables-focused electricity producers Boralex and Northland Power, both of Canada, are among those developing complementary grid-scale storage capacity.

Source: BloombergNEF, October 2023.

| Region | GW | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| China | GW | 1.4 | 2.5 | 5.7 | 20.7 | 24.4 | 30.2 | 28.8 | 30.4 | 32.4 | 34.8 | 37.8 |

| US | GW | 1.4 | 4.1 | 4.6 | 9.6 | 13.5 | 14.3 | 16.3 | 17.1 | 16.2 | 16.8 | 17.0 |

| Europe | GW | 1.3 | 2.3 | 4.0 | 6.8 | 7.4 | 9.8 | 12.7 | 14.9 | 17.2 | 21.1 | 25.8 |

| Rest of the World | GW | 2.0 | 1.4 | 2.1 | 4.8 | 12.0 | 14.7 | 15.5 | 15.8 | 18.9 | 24.2 | 29.7 |

| Total | GW | 6.1 | 10.2 | 16.4 | 41.9 | 57.3 | 69.1 | 73.3 | 78.2 | 84.6 | 96.9 | 110.3 |

Source: BloombergNEF, October 2023.

Overview: This stacked bar chart illustrates the projected rise in new energy storage capacity, by region, each year between 2020 and 2030.

Category one: China

Category two: US

Category three: Europe

Category four: Rest of the World

Overall, the chart shows that additional energy storage capacity is forecast to rise year-on-year in all major regions.

Presentation

This stacked bar chart shows an upward trend across regions in new energy storage capacity this decade.

Longer term, there is a growing need for long-duration energy storage, able to provide power at scale over days and weeks. Here, in addition to the well-established technology of pumped hydroelectricity, companies are placing big bets on electricity conversion. Notwithstanding the energy losses inherent in these transformations, it has been projected that ‘power-to-X’ technologies could reduce global GHG emissions by more than 20% by addressing emissions from hard-to-abate industries (including steelmaking, cement and shipping) and low-temperature heating.18

Tackling bottlenecks in the clean energy transition

The compelling economics of renewable power has pushed the world past the point of no return when it comes to grid transformation. In many markets, it is now cheaper to build new renewables and storage than to operate existing coal-fired plants.19

But the bottlenecks in connecting cheap supply to growing demand will not resolve themselves. Grid constraints are already delaying renewable energy development around the world: 1,500GW of renewables projects in advanced stages of development are stuck in grid connection queues.20

Fortunately, we see renewed focus by governments on plugging the gaps in market incentives and regulatory design needed to redirect capital towards the electricity value chain. In the US, final rulings are expected from the Federal Energy Regulatory Commission this year on proposed changes to regional transmission planning and cost allocation, as well as siting of transmission line routes. The US Department of Energy has recently opened a second round of financial support to regional transmission within a US$2.5bn program authorised by the Inflation Reduction Act.

In Europe, new grid financing mechanisms are anticipated this spring, following the announcement in November 2023 of an EU action plan to accelerate grid build-out between and within member states. Meanwhile in Asia, the Global Energy Interconnection initiative continues to reflect China’s ambition to connect the greater Asia region, via ultra-high-voltage power transmission lines, and become the largest exporter of clean power globally.

The price competitiveness of renewable power generation, combined with widespread policy support, market incentives and improvements in technology, will spur a rapid and sustained rise in investments in grid infrastructure. Such momentum creates opportunities for companies at the forefront of this trend, from grid operators to suppliers of critical and emerging technologies to the industry.

1 IEA, 2023: World Energy Investment 2023

2North American Electric Reliability Corporation, December 2023

3 BloombergNEF, 2023

4 IEA, November 2023: Electricity Grids and Secure Energy Transitions

5 Energy Transition Commission, 22 November 2023: Barriers to Clean Electrification – Grids: the critical gap, presentation to Commissioner meeting

6 Ziegler, B., 5 February 2023: Can the Power Grid Handle a Wave of New Electric Vehicles? Wall Street Journal

7 Peacock, M., Fragaki, A. & Matuszewski, B., 2023: The Impact of Heat Electrification on the seasonal and interannual Electricity Demand of Great Britain. Applied Energy

8 SSE, 15 November 2023: SSE confirms increase to capital investment plan and re-iterates its strong growth prospects

9 BloombergNEF, 8 March 2023: A Power Grid Long Enough to Reach the Sun Is Key to the Climate Fight

10 European Council on Foreign Relations, October 2023: Gridlock: Why Europe’s electricity infrastructure is holding back the green transition

11 US Energy Information, 2022: U.S. electricity customers averaged seven hours of power interruptions in 2021

12 Xodus, 2023

13 Bloomberg data, February 2023

14 Czapla, E., August 2021: The Cost of Upgrading Electric Distribution. American Action Forum

15 IEA, 2023: Deployment to date of residential smart meters, 2021. The share represents the smart meters as a proportion of total electric residential meters.

16 IEA, 2023: Smart Grids

17 BloombergNEF, 9 October 2023: 2H 2023 Energy Storage Market Outlook

18 Israel, H., et al, September 2020: The Special 1 – Hydrogen primer, BofA Global Research

19 Energy Innovation Policy & Technology, January 2023: Coal Cost Crossover 3.0: Local Renewables Plus Storage Create New Opportunities For Customer Savings And Community Reinvestment

20 IEA, 2023: Electricity Grids and Secure Energy Transitions

References to specific securities are for illustrative purposes only and should not be considered as a recommendation to buy or sell. Nothing presented herein is intended to constitute investment advice and no investment decision should be made solely based on this information. Nothing presented should be construed as a recommendation to purchase or sell a particular type of security or follow any investment technique or strategy. Information presented herein reflects Impax Asset Management’s views at a particular time. Such views are subject to change at any point and Impax Asset Management shall not be obligated to provide any notice. Any forward-looking statements or forecasts are based on assumptions and actual results are expected to vary. While Impax Asset Management has used reasonable efforts to obtain information from reliable sources, we make no representations or warranties as to the accuracy, reliability or completeness of third-party information presented herein. No guarantee of investment performance is being provided and no inference to the contrary should be made.